For the past two years, the AI trade was almost embarrassingly straightforward. Buy the brains. Buy the GPUs. Own the companies building the most powerful chips and let the training arms race do the rest. That strategy worked beautifully, and investors who leaned into names like NVIDIA and AMD were rewarded handsomely.

But cycles evolve. They do not ring bells when they shift, and they rarely reward those who stay anchored to yesterday’s winners.

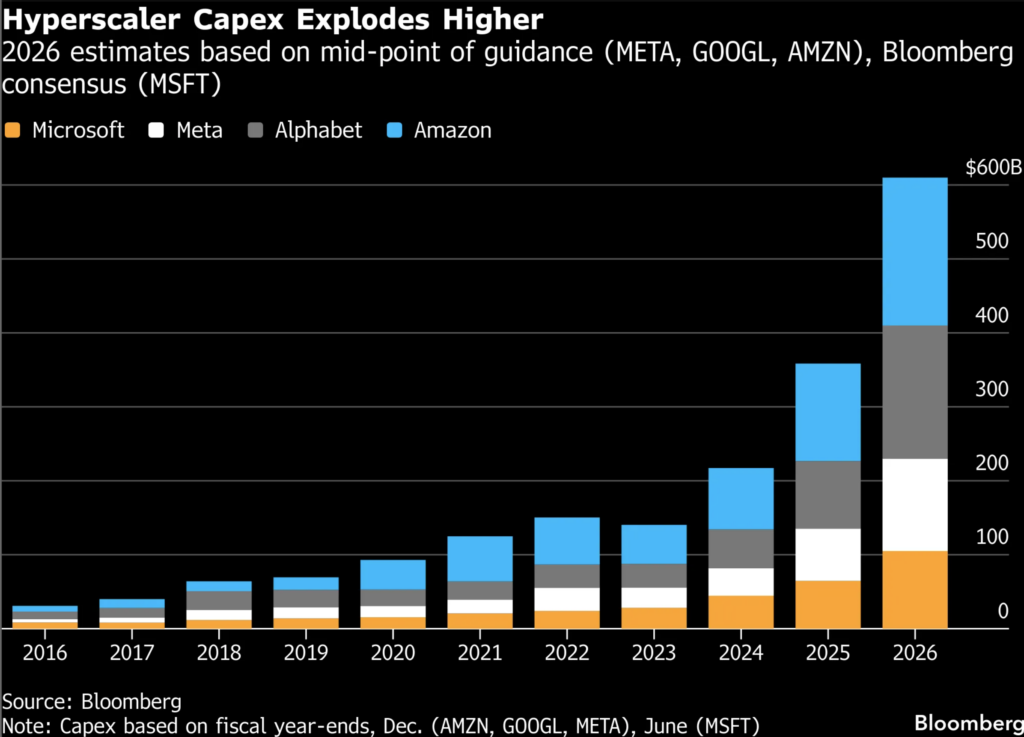

We are now entering a different phase of the AI buildout. Hyperscalers including Microsoft, Amazon, Alphabet, Meta Platforms and Oracle are projected to spend roughly $660 to 690 billion in capex in 2026. That is nearly triple 2024 levels. The first wave of that capital chased compute. The next wave is chasing connectivity, power density and bandwidth efficiency.

In simple terms, we are rotating from buying the brain to buying the bloodstream. The limiting factor in modern AI clusters is no longer just how many accelerators can be installed. It is how quickly those accelerators can communicate, how much energy that communication consumes and how far copper can realistically stretch before physics pushes back. Light, not electrons, is increasingly the answer.

The Hidden Bottleneck: Moving Data at Light Speed

The AI cluster of 2026 does not look like a single monolithic machine. It looks like thousands of GPUs stitched together across racks, rows and buildings, behaving as one distributed system. That stitching is the real choke point. Copper interconnects are running into thermal and bandwidth ceilings. Energy consumed just to move bits around is becoming a material share of total system cost.

This is why silicon photonics has moved from a niche telecom technology into the center of AI infrastructure. Analysts now estimate that more than half of optical transceivers shipped by 2026 could be silicon photonics based, up sharply from roughly one third in 2024. The silicon photonics market itself is expected to grow at a compound rate above 25% through the end of the decade.

You can already see this shift in corporate behavior. Tower Semiconductor has deepened its silicon photonics push and partnered with NVIDIA around advanced optical modules. Coherent and Lumentum are investing aggressively in high speed lasers and optical engines. The conversation in hyperscale architecture circles increasingly frames optical networking as the new AI bottleneck.

I see this as a structural pivot, not a tactical trade. When the constraint in a system shifts, capital follows that constraint. We are moving from a compute bound world to a bandwidth and power bound world. That subtle change alters where the most asymmetric opportunities may sit.

The Three-Phase Rotation

The AI infrastructure buildout follows a predictable capital allocation sequence, just like every prior technology cycle (mainframes → PCs → internet → mobile → cloud):

Each phase doesn’t replace the prior one, it adds a new layer of spending. GPU capex isn’t declining; it’s just growing slower than the optical layer that enables those GPUs to actually communicate. By 2026, over 55% of AI infrastructure spend is dedicated to inference (running models), not training and inference is fundamentally a networking and data-movement problem, not a compute problem.

This is why the “Inference Inflection” is the single most important concept for understanding where photonics capital flows next.

| Phase | Period | Dominant Spend | What’s Bottlenecked | Winners |

|---|---|---|---|---|

| 1 | 2023–2024 | GPUs & accelerators | Raw compute (training) | NVDA, AMD, AVGO |

| 2 | 2024–2025 | Networking + custom ASICs | Fabric bandwidth, inference scale | MRVL, AVGO, LITE, COHR |

| 3 | 2025–2027 | Optical interconnect & SiPh | Data movement energy & density | Supply chain layers 0–6 |

| 4 | 2027–2028 | CPO + optical I/O integration | Chip-level photonic integration | Foundries, packaging, ELS lasers |

Every photonic interconnect, from the 800G transceivers shipping today to the 1.6T CPO modules ramping in 2026 is built through a stack of 9 distinct manufacturing layers. Capital and margin concentrate differently at each layer, and the “discovery” trade rotates up through the stack over time:

Layers 0–2 (Red: Materials → Substrates → Epitaxy) are where the earlier AXTI thesis lives. These are the feedstock layers — low volume, high criticality, extreme concentration. The market discovered Layer 0–1 (AXTI) in late 2025. Layer 2 (IQE, epitaxy) remains undiscovered by US markets.

Layers 3–5 (Teal: Lasers → SiPh Foundry → Test) are the manufacturing layers. This is where the photonic BOM gets fabricated. Capital is flowing here NOW — Tower Semiconductor is tripling SiPh capacity, GlobalFoundries acquired AMF to become the largest pure-play SiPh foundry, Coherent is building the world’s first 6-inch InP laser fab. These are the names the Street is beginning to cover but hasn’t fully priced.

Layers 6–8 (Blue: Packaging → Modules → Systems) are the integration layers. This is where the end-product gets assembled and deployed. Fabrinet, Lumentum, Coherent, and the hyperscalers themselves operate here. These are generally well-covered, the alpha was in 2024–2025.

The Next Rotation: What Gets Repriced in the Next 3–12 Months

Applying the discovery rotation framework and the capital flow data, here’s the sequencing:

Now → Q2 2026: Layer 2–3 Discovery (Epitaxy + Merchant Lasers)

The market has priced Layer 0–1 (AXTI) and is pricing Layer 4 TSEM, GFS. The gap is Layer 2 (epitaxy) and Layer 3 (merchant CW lasers). These are the layers where:

- IQE sits as a monopoly-scale epiwafer supplier invisible to US capital

- MACOM MTSI – is quietly qualifying CW lasers that feed the entire SiPh ecosystem

- Lumentum LITE – still a major merchant laser supplier, especially as ELS ramps.

- Coherent COHR – vertically integrated, but sells merchant lasers too.

Q2–Q4 2026: Layer 5 Inflection (Test & Burn-In)

As SiPh production volumes step-function from qualification to mass production, Aehr Test Systems AEHR becomes the gating factor. Every PIC must be wafer-level burned in before shipping. Their lead SiPh customer has “firmed up production ramps”, orders are expected in calendar 2026.

Additional test players:

Teradyne TER – broader SoC/ASIC test, less pure but still relevant.

FormFacto FORM – probe cards, optical test for SiPh (Keystone Photonics acquisition).

Q3 2026 → 2027: Layer 6 Emergence (Packaging & CPO)

The transition from pluggable optics to co-packaged optics (CPO) is the next architectural shift. CPO integrates the optical engine directly onto the chip package, requiring entirely new packaging approaches. This benefits:

- POET Technologies POET (optical interposer eliminates active alignment)

- Aeluma ALMU is trying to do III–V-on-silicon heteroepitaxy: grow InP/GaAs devices directly on silicon wafers at scale.

- Fabrinet (contract assembly for CPO modules)

- TSMC TSM (COUPE packaging platform for NVIDIA)

2027–2028: Layer 3 Deepening (External Laser Sources)

As CPO matures, the industry moves to an External Laser Source (ELS) architecture — separating the laser from the PIC for thermal and reliability reasons. This creates a massive new socket for standalone CW laser modules, directly benefiting MACOM, Coherent, and Lumentum. This is when Layer 2 (IQE epiwafers) becomes the volume bottleneck, not just a strategic one.

The Photonics Stack Beneath the Headlines

Most investors stop at the module level. They know the optical transceiver vendors. Fewer trace the stack downward into materials, epitaxy, masks and test. That is where the less crowded opportunities often hide. At the substrate level, companies like AXT supply indium phosphide wafers, a key input for high performance lasers. As demand for InP based devices rises, upstream leverage increases almost by default.

Move one layer up and you reach epitaxy, where crystalline layers are grown on those substrates. IQE plc sits here as a leading independent epiwafer supplier. With annual revenue around the high double digit million pound range and a market capitalization not far above that, the valuation reflects stress more than strategic importance. The company has been in a formal strategic review, and in my view, that creates a binary setup. If photonics volumes scale meaningfully, epitaxy capacity becomes mission critical.

Then there are merchant laser and detector suppliers such as MACOM Technology Solutions. Management recently highlighted validation progress for continuous wave lasers targeting 1.6T applications. Data center growth guidance has been lifted into the mid to high 30% range. This is not a speculative science project. It is production level integration into next generation modules.

Further downstream, test and mask suppliers quietly collect tolls on every design. Aehr Test Systems focuses on wafer level burn in, including silicon photonics devices. Photronics supplies advanced photomasks used in logic and increasingly in photonics designs. These are not glamorous businesses, but when volumes ramp, yield and reliability become non negotiable. That is when test and mask intensity rises.

What I find interesting is that the market has already “discovered” certain substrate plays. The next logical rotation, if the thesis holds, moves into epitaxy, lasers and enabling infrastructure. These layers are less visible, yet indispensable.

Positioning in a Rotating Cycle

From a portfolio construction perspective, this is not an argument to abandon the obvious leaders. Broadcom remains deeply embedded in networking and custom silicon. Microsoft and Amazon will continue to benefit from owning the demand side of AI workloads.

However, risk/reward has shifted at the margin. When forward sales multiples stretch into triple digits for certain AI darlings, the asymmetry compresses. Meanwhile, mid cap photonics suppliers often trade at low double digit earnings multiples or low single digit sales multiples despite sitting on structural growth paths tied directly to AI cluster scaling.

I think the smarter framing is not “which GPU wins” but “which function is irreplaceable.” No optical interconnect means no efficient AI cluster at scale. No epitaxy means no lasers. No masks or test means no reliable production. These are functional choke points.

That said, the risk profile differs meaningfully across the stack. Smaller material and epitaxy players face balance sheet constraints and customer concentration risk. Merchant laser suppliers must prove sustained design wins rather than one off validations. Equipment names like Aehr Test Systems depend on volume ramps that can slip by quarters.

There is also the macro overlay. If hyperscaler capex growth moderates due to economic slowdown or internal efficiency gains, the second derivative matters. A deceleration in capex growth does not necessarily mean a collapse in photonics demand, but it could compress multiples before fundamentals catch up.

Still, I believe the structural case is strong. AI clusters are scaling not linearly but exponentially in complexity. Every incremental GPU added to a distributed system increases interconnect demand disproportionately. That dynamic favors bandwidth enablers over time.

Takeaway

The AI trade is not ending. It is maturing. We are moving from buying compute to buying connectivity. I see photonics, optical interconnects and their upstream supply chains as the next logical beneficiaries of hyperscale capex rotation. The market has priced the brains. The bloodstream may be next.