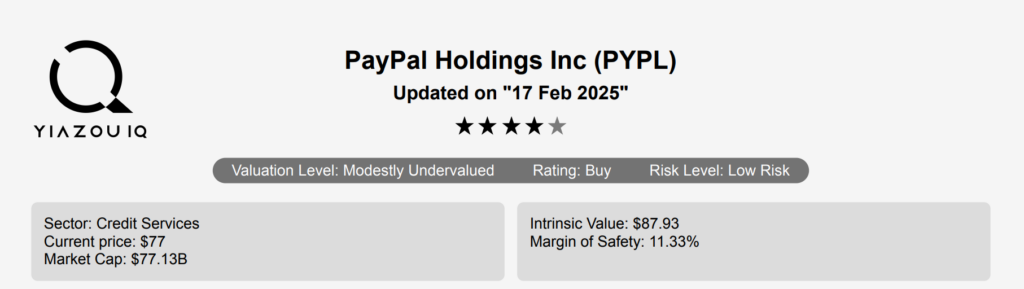

PayPal’s Market Position and Business Model

PayPal (PYPL) was spun off from eBay in 2015 and provides electronic payment solutions to merchants and consumers, with a focus on online transactions. The company had 426 million active accounts at the end of 2023. The company also owns Venmo, a person-to-person payment platform. Currently, PayPal stock is trading at nearly $78.

PayPal’s 10-Year CAGR and Future Revenue Projections

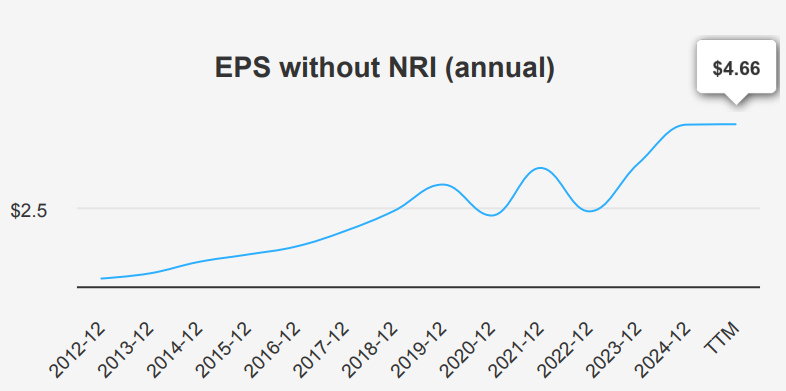

PayPal reported its latest quarterly earnings with an EPS without non-recurring items (NRI) of $1.19, consistent with the previous quarter but showing a notable increase from $1.068 in the same period last year. On a diluted basis, EPS was $1.11, up from $0.99 in Q3 2024, though down from $1.29 in Q4 2023. Revenue per share also grew to $8.267 from $7.663 in Q3 2024, reflecting strong business momentum. Over the past five years, PYPL’s EPS has grown at a compound annual growth rate (CAGR) of 9%, further accelerating to 13.5% over ten years. The industry outlook suggests a steady growth forecast of approximately 10% annually over the next decade.

The company’s gross margin stands at 46.1%, slightly below its 5-year median of 50.05% and significantly lower than the 10-year high of 63.03%. This indicates some pressure on profitability margins, possibly due to increased competition and operational costs. PYPL’s aggressive share buyback strategy has helped bolster its EPS, with a one-year buyback ratio of 7.4%, meaning 7.4% of the shares outstanding were repurchased, a substantial increase compared to its 10-year median of 0.85%. This strategy supports EPS growth by reducing the number of shares outstanding, thereby increasing earnings per share for existing shareholders.

Looking forward, analysts estimate a revenue increase of $33,030.7 million by 2025, with further growth to $37,576.5 million by 2027. EPS estimates for the next fiscal years are $4.863 and $5.416, indicating a robust growth trajectory. The next earnings release, expected on April 30, 2025, will provide further insights into the company’s performance and future guidance.

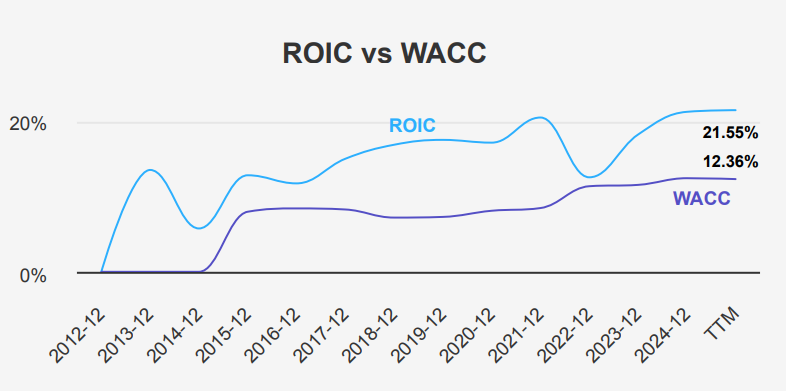

Strong ROIC vs. WACC Signals Positive Value Creation

PayPal stock demonstrates strong financial efficiency and value creation, as evidenced by its Return on Invested Capital (ROIC) compared to its Weighted Average Cost of Capital (WACC). Over the past five years, PYPL has maintained a median ROIC of 18.30%, significantly exceeding its median WACC of 11.41%. This indicates that the company is generating positive economic value by efficiently using its capital to generate returns well above its cost of capital.

Currently, PYPL’s ROIC stands at 21.55%, while its WACC is 12.36%. This further underscores the company’s ability to create shareholder value as it continues to generate returns that are 9.19 percentage points above its cost of capital. The consistently high ROIC relative to WACC highlights PYPL’s strategic capital allocation and operational efficiency.

Overall, PayPal’s performance indicates a robust capability to create economic value, suggesting strong management and effective deployment of resources. This financial strength is crucial for sustaining long-term growth and delivering shareholder value.

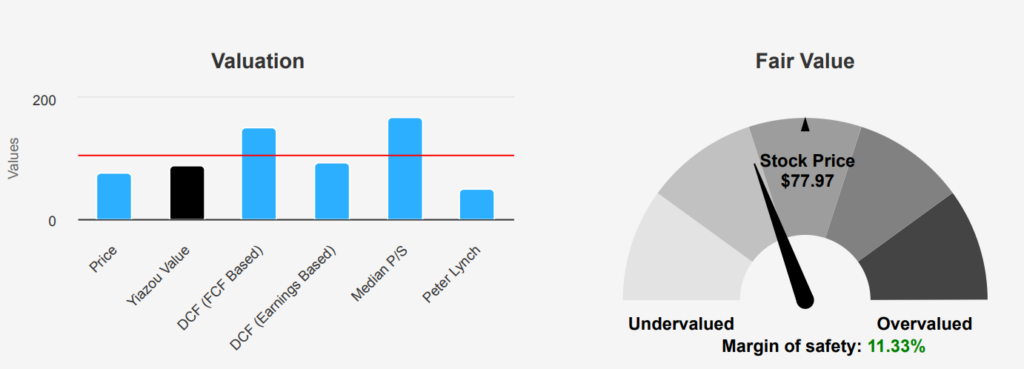

PayPal Stock Trades 11.33% Below Intrinsic Value

PayPal stock currently trades at $77.97, below its intrinsic value of $87.93, offering a margin of safety of 11.33%. This suggests the stock is undervalued relative to its inherent worth, presenting a potential buying opportunity. The Forward P/E ratio of 15.47 is significantly below its 10-year median of 44.49, indicating a more favorable valuation compared to historical norms. Meanwhile, the TTM P/E ratio of 19.44 is on the lower end of its 10-year range, further supporting the case for undervaluation.

Examining the TTM EV/EBITDA ratio at 11.3, it is near the lower spectrum of its 10-year range (Low: 8.10, Median: 24.80), suggesting that the company may be trading at a discount relative to its enterprise value and earnings. The TTM P/B ratio of 3.79 is also below the 10-year median of 4.98, reinforcing the view that PayPal is priced attractively in terms of its book value. The TTM P/S ratio of 2.54 is slightly above its 10-year low of 1.94 but well below the median of 5.36, indicating a favorable price relative to sales.

Analyst ratings and price targets suggest a positive outlook, with a recent target of $94.77, indicating potential upside from current levels. Over the past few months, target prices have remained stable, reflecting confidence in PayPal stock’s prospects despite market volatility. Given these factors, PayPal appears to be undervalued, providing investors with a reasonable margin of safety and an attractive entry point based on its fundamentals and analyst consensus.

Debt, Margins, and Financial Health Indicators

PayPal stock presents a mixed risk profile based on recent financial metrics. The company’s long-term debt has increased by $2.1 billion over the past three years, though it remains at an acceptable level. However, the declining gross margin, with an average annual decrease of 4%, suggests potential challenges in maintaining profitability. The Altman Z-score of 2.03 places the company in the grey zone, indicating moderate financial stress that could increase risk if it declines further.

On the positive side, PayPal’s Piotroski F-Score of 7 reflects strong financial health, signaling efficient use of assets and profitability. The company’s expanding operating margin indicates improved operational efficiency, which is typically a positive indicator of future earnings potential. Additionally, the Beneish M-Score of -2.61 suggests a low likelihood of earnings manipulation, adding a layer of confidence in financial reporting. PayPal’s predictable revenue and earnings per share growth further reinforce its stability.

In conclusion, while PayPal demonstrates several strengths, investors should be mindful of its financial stress signals and declining gross margins. Continuous monitoring of its debt levels and profitability trends is advised to manage potential risks effectively.

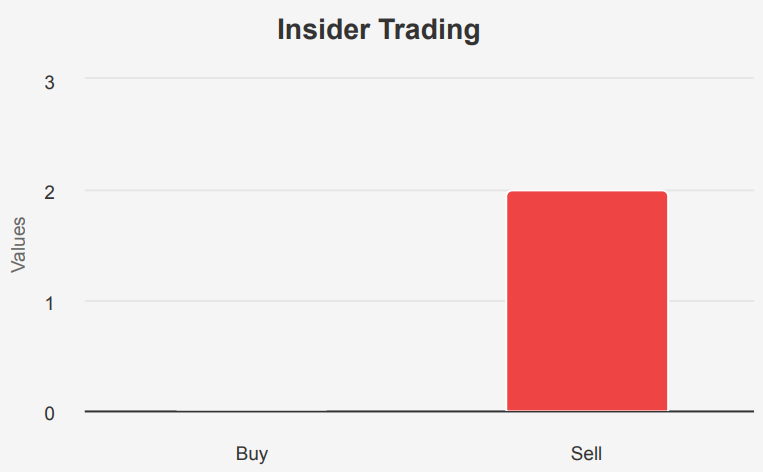

PayPal Stock: No Insider Buying, Institutional Confidence Remains High

In reviewing the insider trading activity for PayPal stock over the past year, it is notable that there have been no insider purchases and only two insider sales within the last 12 months. This lack of buying activity suggests a cautious or neutral stance from insiders regarding the company’s future prospects. The absence of activity in the last 3 and 6 months further indicates stability or possibly a lack of confidence in immediate near-term growth.

Insider ownership stands at 7.26%, which reflects a moderate level of investment by insiders in the company, aligning their interests with shareholders. Meanwhile, institutional ownership is significantly higher at 70.73%, indicating strong confidence from institutional investors in the company’s long-term potential.

The overall trend suggests that while insiders may not be actively buying, they are not significantly divesting either, pointing to a potentially steady outlook from those closest to the company’s operations. Institutional investors’ substantial stake reinforces this perspective, possibly indicating belief in the company’s strategic direction and market position.

Stable Volume, Dark Pool Insights, and Market Trends

PayPal stock has recently exhibited a daily trading volume of ~10,466,960 shares, which is slightly below its two-month average daily trading volume of 10,605,463 shares. This indicates a marginally lower current trading activity compared to the recent average, potentially reflecting either a temporary lull in investor interest or market factors impacting trading.

The Dark Pool Index (DPI) for PYPL stands at 32.88%, suggesting that a significant portion of its trading is occurring off-exchange. A DPI below 50% generally indicates that more trades are happening on public exchanges rather than in dark pools. This could imply increased transparency for PYPL’s trading activities, as a higher proportion of trades are subject to public market scrutiny.

The liquidity situation for PYPL appears stable, given that its trading volume aligns closely with its recent averages. However, the slightly lower current trading volume could warrant monitoring to see if this trend persists, which might affect liquidity and the ease with which investors can enter or exit positions without impacting the stock price significantly. Overall, PYPL maintains a robust trading presence with sufficient liquidity to support ongoing investor interest.

Lawmakers’ Investments Signal PYPL Stock Underperformance

The recent trades in PayPal stock by Representatives James Comer and Josh Gottheimer show differing outcomes. On January 2, 2025, James Comer, a Republican in the House of Representatives, purchased PYPL shares valued between $1,001 and $15,000. As of the report dated January 10, 2025, this investment had an excess return of -13.85%, compared to the SPY, which increased by 4.32% in the same period. This indicates a significant underperformance relative to the broader market.

Similarly, on October 24, 2024, Josh Gottheimer, a Democrat in the House, also purchased shares in PYPL valued in the same range. By November 6, 2024, the excess return was -9.50%, with the SPY gaining 5.30% in the corresponding period. Both trades reflect a challenging environment for PYPL, as both representatives experienced negative excess returns, indicating PYPL’s underperformance against the SPY benchmark.

Disclosures:

Yiannis Zourmpanos has a beneficial long position in the shares of PYPL either through stock ownership, options, or other derivatives. This report has been generated by our stock research platform, Yiazou IQ, and is for educational purposes only. It does not constitute financial advice or recommendations.