- Archer spent $357.7 million on R&D in 2024, with over 70% of operating costs dedicated to product development.

- The company ended Q1 2025 with over $1 billion in cash, aided by strategic funding from Stellantis and Boeing.

- FAA type certification is progressing, with UAE commercial operations set to launch in 2025 via partnerships with regional airlines.

- Stellantis will fund up to $370 million in manufacturing labor, enabling Archer to scale production to 650 units annually.

- Market cap remains ~$5–6 billion, despite Archer targeting a share of a projected $1 trillion urban air mobility market.

The Founder Effect: Culture, Cadence, and Compounding Innovation

Archer’s (ACHR) foundation is unmistakably founder-led. Co-founder and CEO Adam Goldstein, who previously built and sold a software startup to Adecco, brings Silicon Valley agility to this aerospace venture. He and the team have cultivated a “curious, talented, and passionate” culture, emphasizing creative iteration to tackle eVTOL’s engineering challenges. This ethos isn’t just rhetoric: Archer explicitly credits its team and culture as a “key driver of our long-term success.” Such internal tempo, where rapid decision-making and customer-focused innovation echo Amazon’s early playbook, is a hallmark of potential parabolic performers.

Execution cadence at Archer has been striking. Founded in 2018 and emerging from stealth in 2020, Archer unveiled its first demonstrator (“Maker”) in mid-2021 and achieved FAA airworthiness certification plus a hover test flight just six months later. By late 2022, Maker had progressed to full transition flights. This speed, practically unheard of in aerospace, underscores a protocolized, get-things-done mentality akin to Tesla’s fast iteration cycles. Management literally “moved the test team… to a new flight test facility” and stayed “laser-focused” to hit that first flight milestone.

Such protocolization, which includes the the systematizing of processes and knowledge, appears ingrained, from Archer’s safety-first design procedures to its early establishment of a training academy and maintenance operations. (Notably, by early 2024, Archer had already obtained FAA Part 145 certification for maintenance and Part 141 for pilot training, embedding infrastructure for scale before revenues begin.) This level of organizational maturity hints at anti-fragility: Archer is hardwiring lessons and standard procedures now to ensure that as complexity grows, innovation continues to compound rather than becoming bogged down.

In sum, Archer’s leadership model and culture exhibit the traits we associate with durable growth companies: high insider commitment (insiders still own a significant stake, with the founder alone holding a substantial voting share), a bias for action, and proactive system-building. For investors, the litmus test is whether Goldstein’s team can maintain this high-performance rhythm under the strain of ramp-up. If so, Archer’s internal engine could sustain the kind of continuous innovation and resilience that multiplies value over the long run.

Cash, Code, and Capital Cycles: Building the Financial Flywheel

As a pre-revenue disruptor, Archer is in the intensive investment phase of its capital cycle, pouring resources into R&D and manufacturing capabilities ahead of commercialization. The company’s operating expenses have climbed accordingly, with research and development spend rising to $357.7 million in 2024, up from $171.5 million in 2022.

This deliberate cash burn funded the development of the Midnight aircraft and the push for FAA certification. Crucially, Archer has exhibited reinvestment discipline: over 70% of 2024 operating costs went to R&D instead bloated overhead, clearly highlighting that cash is being deployed to build a product and technological moat, not squandered. The revenue trajectory itself remains nascent, meaning that Archer has “not generated revenue” yet from its two planned lines of business and does not expect meaningful sales until its aircraft are certified and in service.

This is a typical profile for a soon-to-be high-growth company, where today’s losses are investments in tomorrow’s cash flow. Investors should expect continuing net losses in the near term (Archer lost $537 million in 2024) but monitor whether those losses begin to plateau as one-time development efforts give way to scalable production.

Despite hefty expenditures, Archer’s financial engine is far from sputtering, thanks in part to savvy capital strategy. The company has raised over $1.1 billion to date, including strategic funding from industry leaders. Notably, automotive giant Stellantis and Boeing have poured in capital, not just as passive investors but as active partners. In 2023, Archer secured a $215 million funding round led by Stellantis, Boeing, United Airlines, and others, bringing total liquidity to over $675 million at that time.

By the first quarter of 2025, Archer’s cash balance surpassed $1 billion, reflecting additional injections and perhaps pre-delivery payments. This war chest provides a healthy runway to reach and scale initial production. Moreover, the Stellantis alliance in particular is a masterstroke in capital cycle management: Archer inked an agreement for Stellantis to shoulder up to $370 million of manufacturing labor costs and $20 million in capex to scale the Midnight factory to 650 aircraft per year.

In exchange, Stellantis earns equity over time, aligning incentives. This deal externalizes a significant portion of production costs, effectively bootstrapping Archer’s manufacturing scale with minimal cash outlay. The result, if executed well, is a classic flywheel: as production volumes rise, unit costs fall, margins expand, and Archer can reinvest cash flows into further growth rather than relying on dilutive capital-raising cycles.

On the “code” front, Archer isn’t just building vehicles. It’s developing complex software, from flight control algorithms to eventually autonomous systems via its partnership with Boeing’s Wisk. This suggests an appreciation that proprietary code and data will be as important as carbon fiber and motors in driving long-term margins. By collaborating with Wisk on autonomy tech, Archer can tap cutting-edge AI without exorbitant in-house spend, essentially outsourcing a major R&D effort in return for equity compensation. It’s a capital-efficient way to future-proof their platform.

From a capital cycle perspective, timing is everything. Archer went public via SPAC in 2021 when market appetite was high, and subsequently raised more funds when its stock was buoyed by strategic news. For instance, its shares jumped 30% on the Boeing alliance news. By leveraging these windows and engaging deep-pocketed partners, Archer has avoided the cash-crunch fate that befell some peers.

Investors should watch whether this financial flywheel truly engages in coming quarters: does Archer continue to hit spending targets and certification milestones without overshooting its budget? Early signs are encouraging, with Q1 2025 spending coming in within guidance. If Archer can manage a transition from cash burn to cash generation by, say, 2026–2027, the groundwork laid today in cash and code will translate into a self-funding growth engine. That is the point at which long-term multiple expansion could really take off.

Moats That Multiply: Defensibility in the Network Economy

Archer isn’t just building a single aircraft; it’s constructing a platform with multiple self-reinforcing advantages. One pillar of its moat is technological IP. The company has filed dozens of patents globally – some with expirations into the 2040s – to protect its designs, ensuring that its years of R&D yield proprietary know-how in areas like battery systems, flight control software, and tilt-rotor configurations.

While aviation patents alone won’t deter determined rivals, they buy Archer time and create licensing opportunities. More compelling is Archer’s budding data flywheel. Every test flight and simulation generates troves of data on aerodynamics, battery performance, noise profiles, and maintenance metrics. Archer’s flight test program has already validated “every hardware and software component” of its demonstrator in hover and transition flight. With each new flight of its Midnight prototypes, the company is learning and iterating.

As the fleet grows (even in test and early service), Archer will accumulate an operational dataset that newcomers can’t easily replicate. This mirrors how Tesla gained an edge in autonomous driving: each additional user improved the system. Archer’s recent partnership with Palantir reinforces this approach, as they are leveraging Palantir’s AI expertise to harness data for “next-gen aviation technologies.”

In practice, this could mean optimized routing algorithms, predictive maintenance models, and autonomous flight training simulations all improving automatically as more Midnight aircraft take to the skies. Usage, in effect, deepens the moat here: more flights equal smarter software and safer, more efficient operations, making Archer’s network more attractive to customers and harder for competitors to catch up to.

Network effects are also evident in Archer’s strategic integrations and partnerships. The company has embedded itself with key incumbents rather than going it alone. Its partnership with United Airlines, which has placed orders for over 100 aircraft and even made pre-delivery payments, not only provides a sales pipeline but also positions Archer within an existing travel ecosystem.

Source: Archer Press Release

United’s passengers could one day seamlessly book an Archer air taxi to the airport, allowing Archer to tap into United’s massive customer base without incurring high customer acquisition costs. This kind of ecosystem lock-in mirrors how Uber leveraged its user base to conceptualize UberAir or how Apple’s App Store makes it difficult for users to switch platforms. Archer is replicating that playbook by forging exclusive relationships.

For example, securing certain “vertiports at key locations” in Los Angeles, including an exclusive deal for the SoFi Stadium site. If successful, these moves ensure that as urban air mobility demand grows, Archer’s aircraft will be the ones flying from prime hubs, reinforcing its market position with each new route.

Crucially, Archer’s moat appears to compound with usage rather than dilute. In traditional aviation, adding more flights can strain infrastructure and erode brand value. But Archer’s model resembles a network tech company: scaling up yields efficiencies and more data, which improve the service, attracting more users in a virtuous cycle. Consider also manufacturing scale: with the Stellantis-backed factory ramping up, producing more units will drive down per-unit costs, allowing Archer to either lower prices or improve margins—again a positive feedback loop.

Early evidence suggests Archer is on track to enjoy cost advantages at scale; they plan to mass-produce Midnight at a rate far above what smaller rivals can do, targeting 650 per year. Competitors like Joby are similarly pursuing scale (with Toyota’s help), but others have struggled. Lilium, for instance, pursued an ambitious but complex jet-style eVTOL; the result has been delays, cash burn, and a collapse in market cap to under $30 million; a cautionary tale of a moat that never materialized.

Archer, by contrast, chose a more pragmatically engineered aircraft. By targeting near-term certifiability and manufacturability, the company shored up its position by allying with giants across auto, airline, and defense sectors. This holistic, “product + network” approach resembles Tesla’s strategy in EVs: integrate hardware and software, build manufacturing prowess, and utilize partnerships (like Panasonic for batteries or now its own charging network) to accelerate adoption. Tesla’s constant innovation made it more resilient than established automakers, and likewise, Archer’s relentless focus on improvement and partnerships could make it more resilient than older aerospace firms entering eVTOL late.

Of course, Archer’s moat will be tested. It operates in an environment where vulnerabilities exist around regulation and technology. For example, certification is a high hurdle that acts as a short-term moat (being one of the first to clear FAA requirements is a huge advantage), but any safety incident post-certification could erode public trust quickly. Additionally, while Archer has exclusive autonomy tech via Wisk/Boeing for future models, rivals like Joby or Airbus’s VX4 could develop their own AI pilots, the tech race remains alive.

Nonetheless, if Archer continues to execute, every new milestone, such as more flight hours, more routes, more data analyzed, will widen the gap between it and the laggards. It’s the hallmark of a sustainable multibagger: a company whose competitive advantages aren’t static, but actually strengthen with scale. Archer’s task is to prove that with each Midnight in the sky, its fortress grows a little taller.

The Inflection Point Nobody Sees: Catalysts Before the Crowd

Archer is approaching a breakout moment by objective measures, even if market perception hasn’t fully caught up. A flurry of early indicators suggests the company is transitioning from development stage to operational readiness. Perhaps most telling is Archer’s human capital surge: its full-time workforce grew by approximately 34% in 2024 to 774 employees (1,148 including contractors).

This hiring momentum, adding top engineers, manufacturing staff, and regulatory specialists, is a classic precursor to commercialization. It signals management’s confidence in imminent certification and production ramp, akin to a tech startup staffing up before a major product launch. Such hiring surges often precede inflection points in output, and in this case, likely foreshadow Archer’s transition from prototype testing to building and operating customer aircraft.

Regulatory milestones are also rapidly accumulating, creating a foundation for Archer’s narrative to pivot. The company achieved its FAA G-1 certification basis approval, establishing the airworthiness standards its eVTOL must meet. With that hurdle passed, Archer has moved into the “Implementation Phase” of testing and compliance, effectively the home stretch toward full type certification.

Each quarter, management updates a checklist of certification tasks accomplished, bringing Midnight closer to FAA approval for commercial flights. Archer is not stopping at U.S. borders, either. International launch preparations are quietly in motion. The company has announced that a UAE launch is on track for later in 2025, with plans to deliver a piloted Midnight aircraft for demo operations during the summer. Its first two “launch edition” customers in the region include Abu Dhabi Aviation and Ethiopian Airlines.

The implication is huge: while many assumed eVTOL would roll out slowly in a few U.S. cities, Archer is positioning globally from day one, targeting geographies eager to leapfrog in urban air mobility. The involvement of the UAE’s General Civil Aviation Authority (GCAA) can be inferred, given that local regulatory approval would be required, a process likely streamlined by the UAE’s proactive approach to aerial taxis. If Archer secures dual certification (FAA and GCAA), it would validate the company’s strategy and likely surprise both competitors and investors.

Catalysts Meet Narrative: The Final Phase of Archer’s Ascent

Archer’s story isn’t just about technology or capital, but also about timing. One key development was Archer’s 2023 settlement with Wisk (Boeing), which not only ended a legal battle but established a partnership for autonomous flight technology. Archer effectively pre-secured the AI pilot for its future aircraft variants, setting the stage for pilotless operations down the line. Initially underappreciated—since the first Midnights will be crewed—this partnership could prove pivotal in a few years.

On the defense front, Archer’s traction is emerging but not yet fully priced in. In July 2024, the U.S. Air Force accepted a Midnight aircraft and began simulating missions, including medical evacuation and surveillance, under a contract worth up to $142 million. This marked not just a financial win but a symbolic one: uniformed personnel operated alongside Archer’s team, underscoring its credibility as a dual-use platform. This broadens the total addressable market beyond civilian transport and provides a hedge against variability in consumer adoption.

All of this foreshadows a narrative shift that is still in its early stages. Despite tangible progress, Archer’s stock has until recently been lumped in with other post-SPAC “story stocks.” That’s beginning to change. After announcing Q1 2025 results and partnerships such as with Palantir for aviation AI, Archer’s stock jumped, lifting its market cap by over 20% in a month. But broader sentiment has yet to reflect the company’s momentum.

The true inflection, where perception meets execution, may not arrive until a Midnight aircraft carries its first commercial passenger or headlines declare “FAA Certifies Archer eVTOL.” By then, the rerating may already be underway. For savvy investors, the opportunity lies in recognizing the transition before it becomes obvious. Archer offers a rare scenario: being “right before right.” The metrics are inflecting, the crowd hasn’t fully noticed, and the multibagger upside lies in that gap.

Valuation Gaps and Virality Triggers: Upside in an Untapped Market

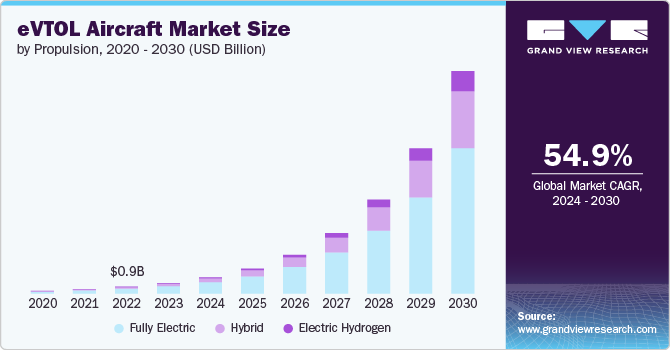

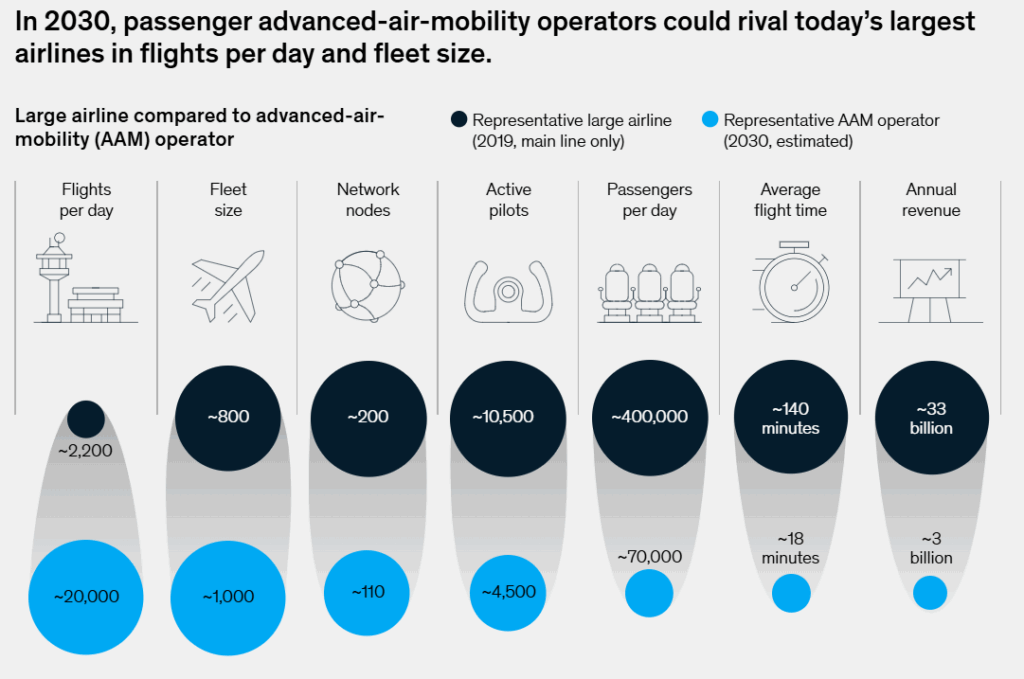

Archer’s current market valuation of around $5–6 billion in mid-2025, reflects a company still priced as speculative, understandable for a pre-revenue firm. Yet that figure appears modest against the backdrop of the total addressable market Archer is angling for. Estimates for the global urban air mobility market run into the hundreds of billions per year in the next 10–15 years; Morgan Stanley, for example, projects a base-case UAM market of roughly $1 trillion by 2040.

Even if such forecasts overshoot and the reality is only a fraction of that, the gap is enormous. Archer’s current market cap is a rounding error in the context of a potential trillion-dollar industry it seeks to help create. This is reminiscent of early Tesla, when its valuation looked absurd relative to its then-tiny revenue, until the EV market exploded and Tesla captured outsized share. Archer does not need to monopolize the UAM market; even a single-digit percentage share of a $100+ billion future market could imply an enterprise value many times the present.

Comparisons to peers also point to a valuation disconnect. Its closest publicly traded peer, Joby Aviation, trades at a similar ~$7–8 billion market cap. Both companies are racing toward first commercial operations. But Archer’s execution and partnership strategy may warrant a premium: it has pulled ahead in areas like manufacturing (via Stellantis) and airline integration, while matching Joby in military collaboration.

Meanwhile, another once-vaunted peer, Lilium, has seen its valuation crater to under $30 million, offering a stark reminder that not all players will make it to the finish line. Archer’s stronger footing suggests it has avoided Lilium’s fate, yet Archer’s valuation hasn’t fully disengaged from the blanket “SPAC discount” the market applied to the whole sector.

As Archer checks off tangible milestones we can expect a valuation re-rating: the market shifting from valuing Archer on vague future hopes to valuing it as an execution story with real cash flows. That shift typically moves the focus from price-to-story to price-to-sales or price-to-EBITDA multiples. And given Archer’s growth potential, those multiples could be generous.

For instance, high-growth aerospace or EV companies in their early breakout years have been valued at 10x, 20x, or higher forward revenues. If Archer approaches even a few hundred million dollars in revenue over the next few years—say, from selling 50 to 100 aircraft and providing operating services, one can envision a market cap far above today’s. In short, significant upside remains if Archer executes, simply by closing the gap between market perception and operational reality.

Beyond fundamentals, one cannot ignore the potential for virality and social sentiment to act as force multipliers for Archer’s stock. This is a company operating at the intersection of cutting-edge tech and sci-fi wonder – “flying cars” – which makes it catnip for retail investors and media hype cycles. We’ve already seen flickers of this: Archer’s association with glamor names like ARK Invest (a major backer in its 2023 PIPE funding) and Cathie Wood’s public enthusiasm for air mobility has drawn in a cadre of futurist investors.

The stock’s massive rise over the past year hints at speculative interest returning as the company proves naysayers wrong step by step. It’s not hard to imagine a scenario where a dramatic catalyst say, the first public eVTOL taxi flights at an international event or a viral video of an Archer Midnight effortlessly zipping over LA traffic captures the public imagination.

In today’s meme-stock era, such moments can trigger virality that sends stocks parabolic, as seen with other disruptive transport names. Archer has multiple shots on goal here: a high-profile strategic announcement (perhaps a partnership with Uber or a large ride-sharing integration) or even a short squeeze given any lingering short interest. We’ve seen single news items cause spikes (e.g., the Boeing/Wisk deal not only de-risked Archer but also “jumped [the] shares 30%” in after-hours trading).

Consider the upcoming catalysts: FAA approval (which would be headline news globally), the first airline customers taking delivery, or new government contracts. Each of these could not only fundamentally justify a higher valuation but also spark a fear-of-missing-out (FOMO) wave among investors. The social momentum around green mobility and tech disruption could amplify a run in Archer’s stock if the narrative flips from “if” to “when.”

In assessing Archer’s valuation today, investors must balance the inherent risks (execution challenges, unproven commercial viability) against the asymmetric upside. The company remains a story in transition, but the conditions for a re-rating are increasingly aligning: improved fundamentals, reduced time to revenue, and a growing stakeholder base from retail traders to institutional giants, all preparing to amplify the story.

If Archer delivers on its milestones and the broader market remains favorable to growth companies, the convergence of internal progress and external enthusiasm could unlock a sharp upward move in valuation. Put plainly, Archer’s stock could lift off from its current base into a much higher orbit, powered by both execution and the compelling narrative of a breakthrough finally realized.

High-Conviction Upside: Watch Catalysts, Mind the Skies

Archer Aviation represents a high-risk, high-reward opportunity with tangible signs of progress. From successful test flights and global partnerships to a fortified balance sheet, the company is graduating into a real business that could reshape urban transport. The next 6–12 months will be critical. Investors should monitor progress on FAA type certification and the launch of commercial operations, including the UAE rollout and any first paying passenger flights. These milestones are the KPIs that will validate Archer’s multibagger thesis.

Given Archer’s momentum and growing competitive moat, the stock is one to accumulate on conviction; albeit with prudent position sizing due to expected volatility. If Archer stays on track with certification and begins scaling deliveries as planned, the bull case would be significantly de-risked. In that case, today’s valuation could prove to be a historical dislocation. Archer may well become a parabolic performer in forward-looking portfolios, offering not just financial upside, but a stake in the future of how the world moves.