ASML: Market Leader in Photolithography Systems for Semiconductors

ASML is the leader in photolithography systems for manufacturing semiconductors. Photolithography is the process in which a light source forces and exposes circuit patterns from a photo mask onto a semiconductor wafer. The latest technological advances in this segment allow chipmakers to continually increase the number of transistors on the same area of silicon, with lithography historically representing a high portion of the cost of making cutting-edge chips. ASML outsources the manufacturing of most of its parts, acting like an assembler. ASML’s main clients are TSMC, Samsung, and Intel. ASML stock is currently trading at ~$756. Let’s explore ASML stock forecast.

29% EPS CAGR and $38.7B Revenue by 2026: ASML’s Growth Story

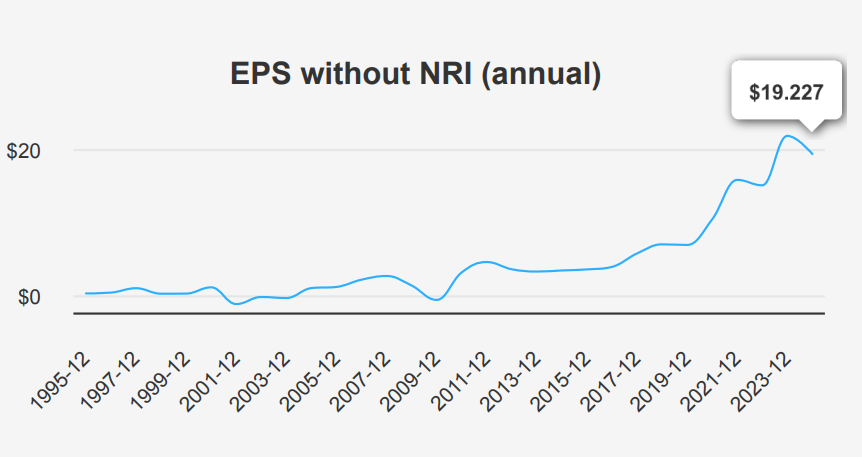

ASML reported a strong Q3 2024 performance, with EPS without NRI (excluding non-recurring items) increasing to $5.86, up from $4.316 in Q2 2024 and $5.133 in Q3 2023. This represents a 35.8% quarter-over-quarter (QoQ) increase and a 14.2% year over-year (YoY) increase. Revenue per share also grew to $21.056 from $17.077 in the prior quarter, reflecting robust demand for ASML’s products. Over the last five years, ASML achieved a 29% CAGR in annual EPS without NRI, underscoring its consistent growth trajectory, while the 10-year CAGR stood at 24%.

The company maintained a solid gross margin of 51.15% in Q3, slightly above its five-year median of 50.54% and significantly higher than the 10-year median of 46.01%. This margin strength highlights ASML’s effective cost management and premium product positioning. ASML’s share buyback ratio over the past year was 0.40%, indicating a moderate repurchase of shares, which supports the EPS by reducing the number of shares outstanding. Over a 10-year period, the buyback ratio averaged 1.10%, reflecting a consistent strategy to enhance shareholder value through share repurchases.

Looking ahead, analysts project revenue to grow steadily, with estimates of $28,949.56 million for the end of 2024, reaching $38,686.31 million by the end of 2026. The estimated EPS for FY1 ending 2025 is $19.733, indicating continued earnings growth. Industry forecasts predict a growth rate of approximately 7% annually over the next decade, driven by advancements in semiconductor technology. ASML’s next earnings release is on January 29, 2025, where further insights into its strategic direction and financial performance under ASML stock forecast.

ASML Stock’s ROIC Exceeds WACC, Ensuring Strong Financial Health

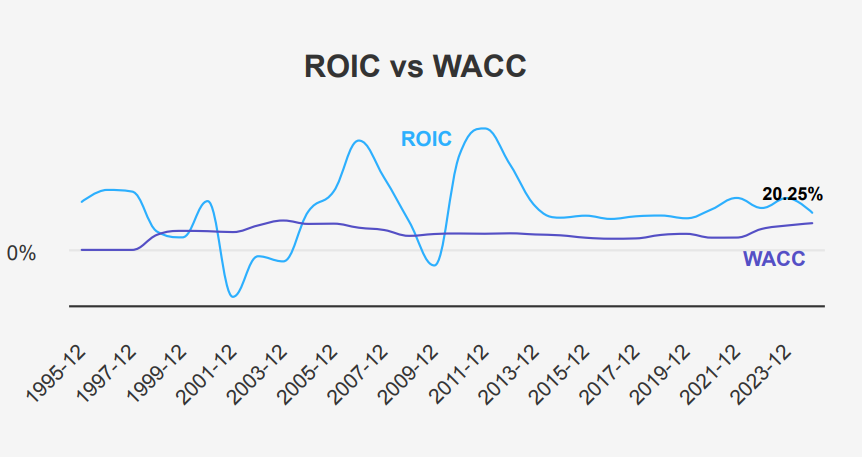

ASML’s financial performance demonstrates strong value creation capabilities, particularly when evaluating its Return on Invested Capital (ROIC) against its Weighted Average Cost of Capital (WACC). Over the past five years, ASML’s median ROIC is 23.53%, significantly surpassing its median WACC of 8.76%. This indicates that ASML has been effectively generating economic value, as its returns on investments are substantially higher than the cost of capital required to fund those investments.

Currently, ASML’s ROIC is 20.15%, still surpassing its WACC of 14.46%, which, despite being the highest in a decade, remains below the ROIC. This continued trend of ROIC exceeding WACC confirms ASML’s ability to create shareholder value consistently over time. The company’s high ROE, at 49.40%, further underscores its efficiency in leveraging equity to generate profits. Overall, ASML demonstrates effective capital allocation and strong financial performance, maintaining a solid track record of generating returns that significantly exceed its cost of capital, indicating sustainable economic value creation.

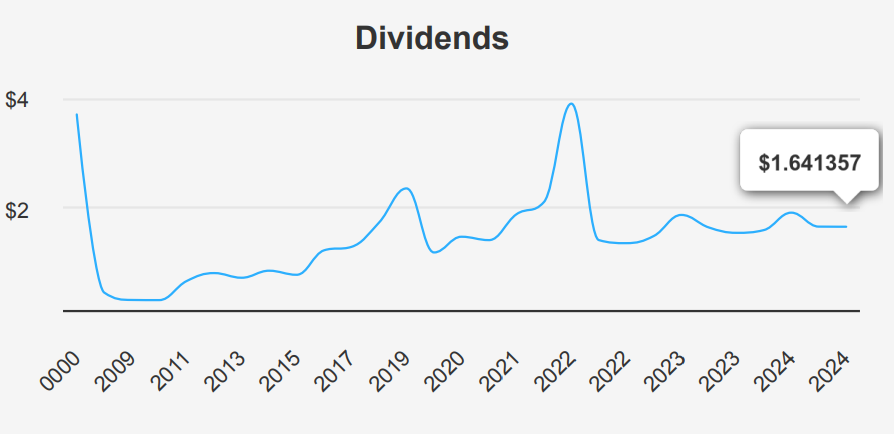

ASML’s Dividend Growth: 14.31% Forecast and Sustainable Payouts

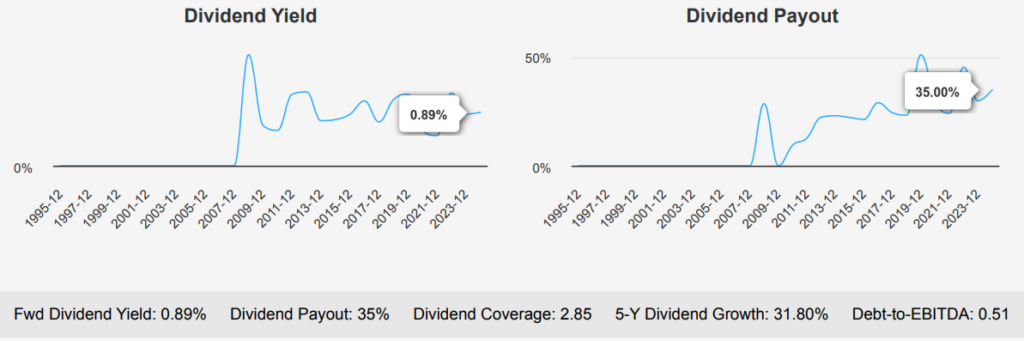

ASML has demonstrated impressive dividend growth, with a 5-year growth rate of 31.80% and a 3-year growth rate of 32.70%. The company’s forward dividend yield stands at 0.89%, slightly above its 10-year median of 0.84% but below the historical high of 1.73%. The dividend payout ratio is currently at 35.0%, indicating a sustainable distribution level compared to its historical highs of around 100%.

The company’s debt-to-EBITDA ratio stands at 0.51, which is well below the threshold of 2.0, suggesting a very low financial risk and a strong capacity to service its debts. This solid financial footing supports sustainable dividend payouts, evidenced by a payout ratio of 35.0%—a conservative figure compared to its historical highs.

Looking ahead, ASML may maintain a robust dividend growth rate of 14.30% over the next 3-5 years. The next anticipated ex-dividend date, based on a quarterly frequency, should fall around January 29, 2025, presuming this date is a future weekday. ASML’s financial health and growth prospects remain attractive within the semiconductor sector, known historically for its resilience and innovation-driven growth.

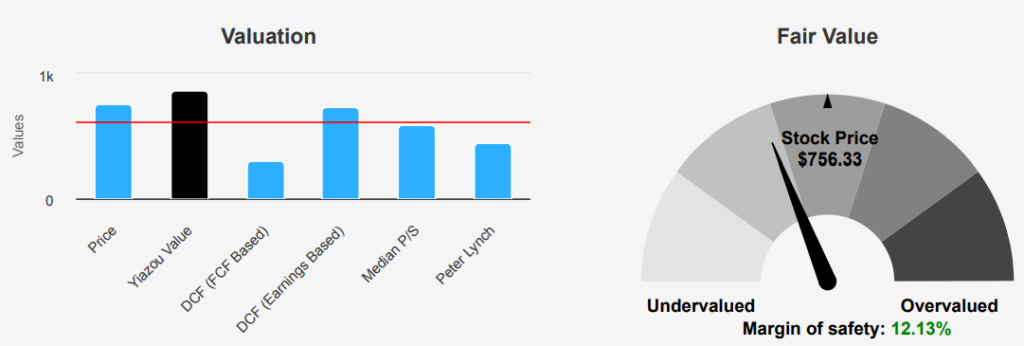

ASML Stock Undervalued by 12% Against Intrinsic Value

ASML’s current stock price of $756.33 is below its intrinsic value of $860.77, suggesting a margin of safety of 12.13%. This indicates that the stock is potentially undervalued, providing a buffer for investors. The Forward P/E ratio is 30.13, which is below the 10-year median of 34.93, suggesting a reasonable valuation relative to its historical context. Conversely, the TTM P/E ratio at 39.34 exceeds the median, indicating potential overvaluation if the company’s earnings growth does not meet expectations.

Examining other valuation metrics, ASML’s EV/EBITDA TTM is 29.75, slightly above its 10-year median of 27.15, indicating a premium valuation compared to its historical averages. The TTM Price-to-Book ratio is significantly high at 18.29 against a 10-year median of 8.66, suggesting the stock may be trading at a substantial premium to its book value. The TTM Price-to-Free-Cash-Flow ratio is notably high at 104.38, far surpassing its median of 42.47, which could signal overvaluation unless future cash flows increase substantially.

Analyst sentiment remains optimistic, with a price target of $919.49, up from $914.85 a week ago, reflecting ongoing confidence in ASML’s growth prospects. However, the gradual decrease from three months ago indicates tempered expectations. Overall, while the intrinsic valuation and analyst targets suggest upside potential, the current premium on key valuation metrics warrants cautious optimism, particularly if market conditions shift or growth projections are not hit under the ASML stock forecast.

ASML: Balancing Revenue Concerns with Strong Financial Metrics

ASML Holding NV’s recent slow revenue growth per share could be a concern for investors, as it might indicate a deceleration in business momentum. However, this needs to be balanced against other positive financial indicators. The company’s Beneish M-Score of -2.22, which is well below the threshold of -1.78, suggests that ASML is not likely engaging in financial manipulation, providing assurance of the integrity of its financial reporting.

Furthermore, ASML’s expanding operating margin signals improved efficiency and profitability, a positive trend that can enhance shareholder value if sustained. The company’s robust financial health is underscored by its strong balance sheet ranking and a high Altman Z-score of 8.39, which indicates a very low probability of financial distress. These factors collectively suggest that despite the recent slowdown in revenue growth, ASML remains fundamentally strong, potentially offering a resilient investment opportunity in the semiconductor industry.

No Insider Trading, 19.37% Institutional Ownership: Stability for ASML

Under ASML stock forecast, analyzing insider trading activities for ASML over the past year reveals no buying or selling actions by insiders, indicating a complete lack of such transactions. With insider buy and sell counts at zero for 3, 6, and 12 months, this absence of activity may suggest a neutral stance by the company’s directors and management regarding the company’s stock performance. Additionally, there is insignificant insider ownership, reflecting that individuals in key positions do not hold any shares, which might be atypical for a company of its stature.

On the other hand, institutional ownership is significant at 19.37%, highlighting a considerable level of confidence by larger financial entities in ASML’s performance and prospects. Institutional investors often conduct extensive research before investing, which could imply a positive outlook on the company’s future. The absence of insider transactions combined with notable institutional engagement might suggest stability but also warrants further investigation into the reasons behind the lack of insider ownership and trading activity.

ASML Stock: High Liquidity and Balanced Dark Pool Activity

ASML stock’s shows robust liquidity and trading activity. The average daily trading volume over the past two months is 1,526,103 shares, indicating steady investor interest in the stock. On the day assessed, the trading volume was notably higher at 1,894,248 shares, suggesting increased trading activity, which could be due to market news or earnings announcements.

The Dark Pool Index (DPI) for ASML is 29.92%. This metric provides insight into the portion of trades occurring in dark pools, which are private exchanges for trading securities. A DPI of 29.92% indicates that a significant portion of ASML’s trading volume is occurring off the public exchanges, which can sometimes reflect large institutional trades seeking to minimize market impact.

Overall, ASML’s trading volume surpassing its 2-month average suggests heightened market engagement, while the DPI percentage points to a substantial level of institutional trading activity. This combination of high trading volume and significant dark pool activity may imply strong market interest and potential volatility, necessitating close monitoring under ASML stock forecast.

Bipartisan Interest: U.S. Representatives Trade ASML Shares in 2024

The recent trading activity in ASML stock by members of the U.S. House of Representatives highlights notable bipartisan engagement with this particular stock. On November 25, 2024, Representative Marjorie Taylor Greene, a Republican, purchased shares valued between $1,001 and $15,000. This transaction was reported shortly after, on November 27, 2024. In contrast, Democratic Representative Jonathan Jackson sold shares in ASML on October 28, 2024, with a transaction value in the range of $15,001 to $50,000, as reported on November 29, 2024.

This exchange of positions suggests differing perspectives or strategic approaches toward ASML’s market potential. Greene’s purchase may indicate confidence in the company’s future prospects, while Jackson’s sale could be aligned with profit-taking or reallocating his portfolio. These trades reflect individual strategic decisions that might be influenced by broader market conditions or personal financial strategies.

Disclosures:

Yiannis Zourmpanos has a beneficial long position in the shares of ASML either through stock ownership, options, or other derivatives. This report has been generated by our stock research platform, Yiazou IQ, and is for educational purposes only. It does not constitute financial advice or recommendations.