Executive Summary

Aehr Test Systems $AEHR is the only company in the world that offers both wafer-level and package-level burn-in for AI processors, silicon photonics, SiC power devices, GaN, and flash memory. The stock sits at $40, trading at the trough of an earnings downcycle driven by SiC/EV weakness while a massive AI and photonics order cycle is just beginning.

With a $14M AI processor order confirmed on Feb 25, 2026, a Sonoma hyperscaler production win on Feb 11, and H2 bookings guidance of $60–80M, the company is transitioning from SiC-dependent cyclical to multi-market AI infrastructure play.

The $1B TAM by 2027 is real, the balance sheet is fortress-clean (zero debt $24.5 cash), and the moat is monopolistic. Consensus analyst estimates are stale at $21 reflecting the old SiC narrative, not the emerging AI thesis. This creates one of the widest perception gaps in the semiconductor equipment space.

What Does AEHR Actually Do?

The Simplest Explanation

When a company like Nvidia, Google, or Amazon builds an AI data center, they install thousands of high-power chips. Each chip costs $10,000–$30,000. If even 1% of those chips fail in the first few months (called “infant mortality”), it can crash an entire rack worth $500,000+.

AEHR makes the machines that catch bad chips before they ship. The process is called “burn-in” essentially stress-testing every chip at extreme temperatures and full power for hours or days, forcing weak chips to fail in the factory instead of in a customer’s data center.

There are two ways to do this:

- Wafer-level burn-in (WLBI): Testing chips while they’re still on the silicon wafer (before cutting them apart). This is cheaper and faster because bad chips can be thrown away before expensive packaging. AEHR’s FOX-XP and FOX-NP systems do this — they can test up to 18 wafers simultaneously, each containing hundreds or thousands of chips.

- Package-level burn-in (PPBI): Testing chips after they’ve been individually packaged. AEHR’s Sonoma systems handle this for ultra-high-power AI ASICs that need 2,000+ watts per device during burn-in.

AEHR is the only company offering both. Advantest and Teradyne make broader test equipment, but neither offers full-wafer burn-in at the power levels AI processors require.

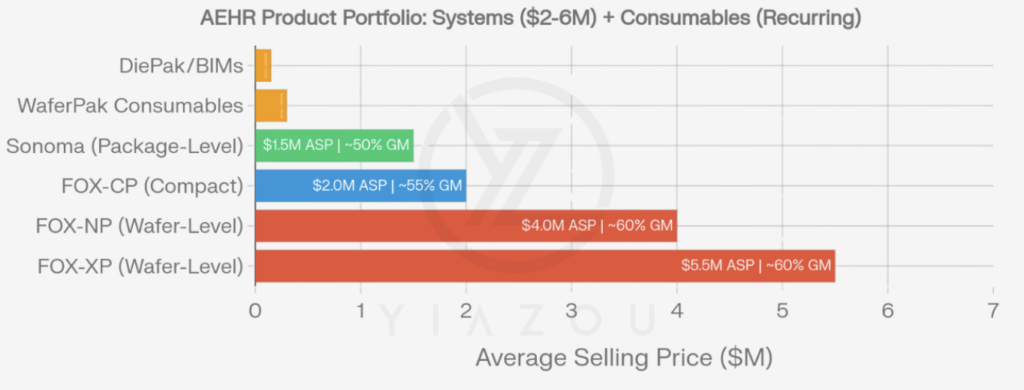

Product Portfolio

| Product | Type | ASP | Margin | Target Market |

|---|---|---|---|---|

| FOX-XP | Wafer-level burn-in | ~$5–6M per system | ~60% | AI processors, SiC, SiPho, memory |

| FOX-NP | Wafer-level burn-in | ~$4M per system | ~60% | AI processors, newer platform |

| FOX-CP | Compact reliability | ~$2M per system | ~55% | Qualification testing |

| Sonoma | Package-level burn-in | ~$1–2M per system | ~50% | AI ASICs (hyperscaler custom chips) |

| WaferPak Contactors | Consumable | ~$300K each | ~70% | Recurring revenue per wafer tested |

| BIMs/BIBs/Sockets | Consumable | ~$100–200K each | ~65% | Recurring revenue per device tested |

The Financial Picture

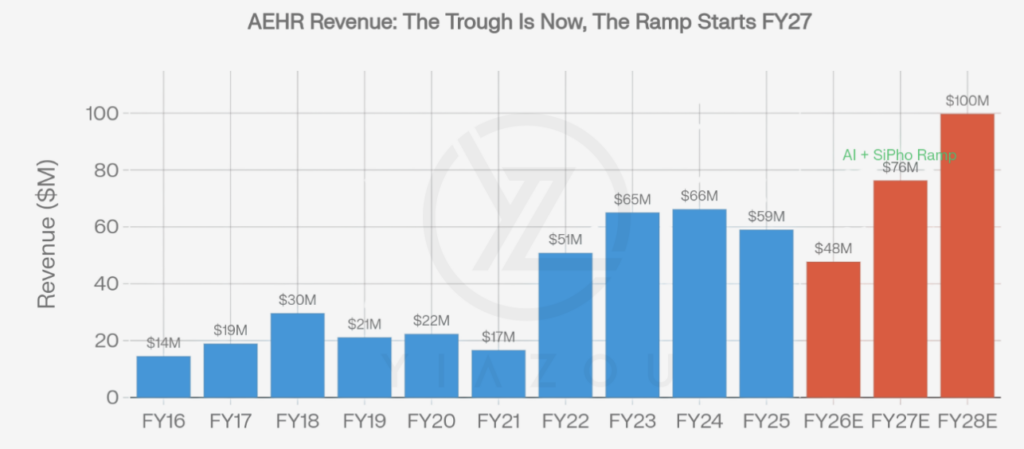

Revenue History: The SiC Trough

AEHR’s revenue tells a clear story of boom-bust-pivot:

AEHR’s revenue tells a clear story of boom-bust-pivot:

- FY16–FY21: Legacy test business, revenue oscillating $15–22M, consistently unprofitable

- FY22–FY23: SiC/EV boom drove revenue to $50.8M → $65.0M, with 50% gross margins and 20%+ operating margins

- FY24–FY25: SiC/EV demand collapsed as auto OEMs delayed EV programs. Revenue fell to $59.0M with margins compressing to 41% gross

- FY26 (current): Q1 revenue $11.0M, Q2 $9.9M — the trough. Gross margins hit 26%in Q2, the lowest in years

The AI Catalyst: Why Everything Changes Now

On February 25, 2026, AEHR received a $14 million production order from its lead AI processor customer for multiple fully automated FOX-XP wafer-level burn-in systems. Key details:

- 9 x 300mm wafers tested in parallel per system, delivering thousands of amperes of current per wafer

- Full automation with WaferPak contactors and automated aligners

- Shipping within 6 months (summer 2026)

- Customer is a manufacturer of AI processors for data center training and inference

- This expands an existing installed base — the customer already as FOX-XP systems; this adds full automation across production lines

CEO Gayn Erickson stated: “We have recently completed a significant facility upgrade, adding power, cooling infrastructure, and cleanroom space that substantially increases our production capacity”.

The Sonoma Hyperscaler Win (Feb 11, 2026)

Two weeks earlier, AEHR secured a production purchase order from a hyperscale data center customer for Sonoma package-level burn-in of their next-generation AI ASIC processor. This customer:

- Is developing proprietary AI accelerator ASICs for training and inference

- Has publicly described plans for “very significant capital expenditures” for AI and data center infrastructure

- Already has a current-generation AI processor in mass production

- Is expected to place considerably more Sonoma orders in H2 2026 and into 2027

The hyperscaler profile (proprietary AI ASIC, massive capex plans, Silicon Valley location) matches companies like Google (TPU), Amazon (Trainium/Inferentia), or Microsoft (Maia).

H2 Bookings Target: $60–80M

Management expects H2 FY26 bookings of $60–80 million, up from ~$20M in H1. This would represent:

- A 3–4x acceleration from H1 levels

- Bookings that exceed full-year FY25 revenue ($59M) in just 6 months

- The foundation for a “very strong fiscal 2027” as bookings convert to shipments

Management has emphasized these are based on specific customer forecasts, not aspirational targets.

The Moat: Why Nobody Can Compete

Monopoly in Wafer-Level Burn-In

AEHR’s competitive position is monopolistic, not just dominant. Here’s why:

- Only full-wafer burn-in solution: Advantest and Teradyne test chips individually or in small groups. AEHR tests entire 300mm wafers (hundreds of chips simultaneously) at full operating power. No competitor offers this.

- Power delivery capability: FOX-XP delivers up to 3,500 watts per wafer and thousands of amperes of current. Modern AI processors require extreme power during burn-in that no other platform can deliver.

- Patented WaferPak contactor: The WaferPak is a full-wafer probe card that makes simultaneous contact with every chip on a 300mm wafer. This is proprietary, patent-protected technology with no equivalent on the market.

- 48 years of accumulated know-how: Founded in 1977, AEHR has spent nearly five decades perfecting wafer-level burn-in. The thermal management, power distribution, and contactor alignment required are extraordinarily difficult to replicate.

- Qualification stickiness: Once a hyperscaler qualifies AEHR’s tools into their production flow, switching costs are enormous — 6–12 months of requalification, potential yield loss, and production delays. No customer would risk this for an unproven alternative.

Competitive Comparison

| Company | What They Do | Overlap with AEHR | Threat Level |

|---|---|---|---|

| Advantest ($5B) | Automated test equipment (ATE) | Tests packaged chips, not wafer-level burn-in | Low — different approach |

| Teradyne ($18B) | ATE, robotics | Broad testing platforms, no full-wafer burn-in | Low — different segment |

| Cohu ($1.4B) | Test handlers, contactors | Handles devices for test, doesn’t burn them in | Low — complementary |

| FormFactor ($3B) | Probe cards | Wafer probing for test (not burn-in) | Low — different function |

None of these companies can deliver full-wafer burn-in at thousands of amperes. They test chips electrically; AEHR stress-tests chips thermally and electrically simultaneously at full operating power. The technologies serve different purposes in the manufacturing flow.

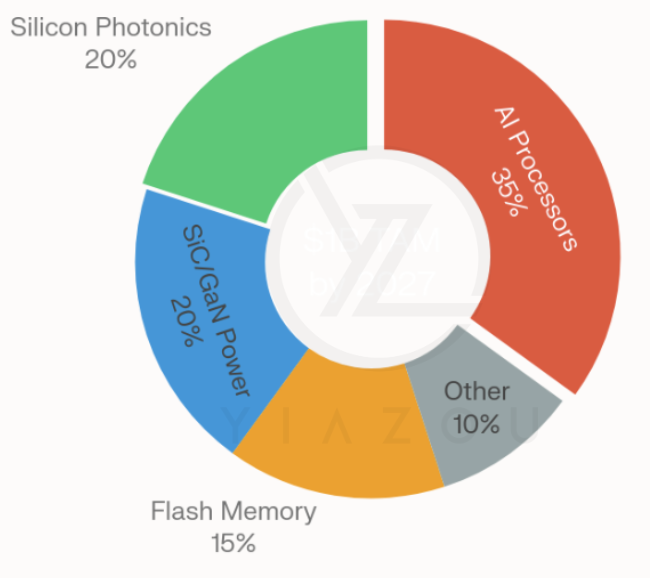

Total Addressable Market: $1 Billion by 2027

AEHR’s management has outlined a $1B TAM by 2027, split evenly between $500M in systems and $500M in consumables. The major segments:

AI Processors (~35% of TAM)

Every major hyperscaler (Google, Amazon, Microsoft, Meta) is building custom AI ASICs, and all of them require burn-in to ensure reliability. AEHR’s current AI customer base includes:

- A lead AI processor manufacturer (FOX-XP production orders, $14M Feb 2026)

- A leading hyperscaler (Sonoma production orders for proprietary AI ASIC)

- A top-tier AI processor supplier (FOX-XP evaluation program since Aug 2025)

- A world-leading OSAT (partnership for advanced AI testing solutions)

Silicon Photonics (~20% of TAM)

AEHR is already in volume production for silicon photonics burn-in. As 800G/1.6T transceiver demand explodes (see broader photonics thesis), the silicon photonics chips inside those transceivers need burn-in testing. This market grows in lockstep with the optical transceiver market.

SiC/GaN Power Semiconductors (~20% of TAM)

The original growth driver. Despite the EV slowdown, SiC is recovering as industrial and grid applications pick up. AEHR secured its first GaN production order from a leading automotive semiconductor supplier, opening a new $2B+ device market growing at 40%+ CAGR.

Flash Memory (~15% of TAM)

A benchmarking project with a major NAND Flash memory supplier is underway using a new fine-pitch WaferPak. The NAND market exceeds $80B annually — a 1% yield improvement represents $800M in value. First revenue could come in FY2027.

Analyst Estimates and Why They’re Wrong

Consensus Is Stale

Only 1 analyst currently covers AEHR with a price target — Craig-Hallum at $21, which is a Hold rating set on January 9, 2026. This target was set before both the Sonoma hyperscaler win (Feb 11) and the $14M FOX-XP order (Feb 25).

| Metric | FY26E (Consensus) | FY27E (Consensus) | FY28E (Consensus) |

|---|---|---|---|

| Revenue | $47.7M | $76.3M | $99.7M |

| Revenue growth | -19% | +60% | +31% |

The FY27E consensus of $76.3 assumes moderate AI ramp-up. But if H2 bookings hit $60–80M as management guides, and those convert to shipments in FY27, revenue could exceed $120–150M — 60–100% above consensus.

Earnings Surprise History

| Quarter | Revenue Actual | Revenue Est. | EPS Actual | EPS Est. | Post-Earnings Move |

|---|---|---|---|---|---|

| Q4 FY24 | $16.6M | $15.4M | $0.81 | $0.11 | +22% |

| Q1 FY25 | $13.1M | $12.2M | $0.04 | $0.01 | +20% |

| Q2 FY25 | $13.5M | $19.7M | -$0.01 | $0.03 | -27% |

| Q3 FY25 | $18.3M | $14.8M | $0.02 | $0.01 | +29% |

| Q4 FY25 | $14.1M | $14.8M | -$0.06 | -$0.01 | -12% |

| Q1 FY26 | $11.0M | $11.1M | -$0.05 | $0.01 | -17% |

| Q2 FY26 | $9.9M | $16.2M | -$0.11 | -$0.08 | +0.16% |

The Q2 FY26 miss ($9.9M vs. $16.2M est.) would normally crash a stock but AEHR was flat post-earnings. The market looked through the miss to the $60–80M H2 bookings guide and the Sonoma orders. This is a classic signal that the bottom is priced in.

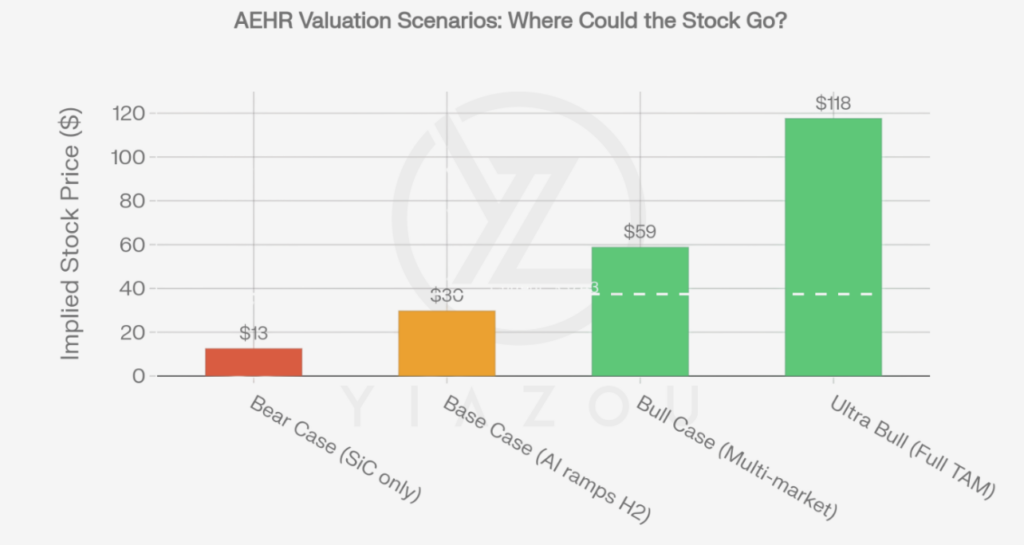

Valuation Framework

Revenue-Multiple Approach

| Scenario | FY27 Revenue | Revenue Multiple | Implied Market Cap | Implied Stock Price | Upside |

|---|---|---|---|---|---|

| Bear (SiC only, AI delays) | $48M | 8x | $384M | ~$13 | -66% |

| Base (AI ramps per guide) | $76M | 12x | $912M | ~$30 | -20% |

| Bull (AI + SiPho + Memory) | $120M | 15x | $1.8B | ~$59 | +58% |

| Ultra Bull (Full TAM capture) | $200M | 18x | $3.6B | ~$118 | +215% |

At $37.43, the stock trades at roughly 15x FY27E consensus revenue of $76.3— reasonable for a monopoly semiconductor equipment company transitioning to AI. But consensus is likely too low by 50–100%.

Cross-Check: Production Capacity Math

AEHR has stated production capacity of ~20 wafer-level systems and ~20 package-level systems per month. At ASPs of $5–6M (wafer-level) and $1–2M (package-level):

- Maximum annual system revenue: (20 × $5.5M × 12) + (20 × $1.5M × 12) = $1.68B

- Even at 10% utilization: $168M annual system revenue

- Plus consumables: 50% of system revenue = $84M

- Total at 10% utilization: ~$252M

Current revenue of ~$48M implies AEHR is running at roughly 3% of capacity. The facility upgrades completed in early 2026 significantly expanded this ceiling further.

Key Risks

Near-Term Risks

- H2 bookings miss: If the $60–80M H2 target doesn’t materialize, the stock revisits $20–25. This is the single largest binary risk.

- Margin recovery delay: If Q3/Q4 FY26 margins don’t revert to 40%+ as systems ship, investor confidence erodes.

- Customer concentration: Revenue appears dependent on 2–3 large customers (lead AI processor maker, hyperscaler, SiC customer). Loss of any one would be material.

Structural Risks

- AI capex slowdown: If hyperscalers cut capital budgets (as in 2022–23), AI processor burn-in demand delays. However, current hyperscaler capex plans for 2026 ($690B+) suggest this is unlikely near-term.

- Burn-in obsolescence: If chip reliability improves enough that burn-in becomes unnecessary. This is extremely unlikely — as chips get more powerful (higher wattage, more complex), burn-in becomes more important, not less.

- IP litigation: AEHR is involved in ongoing IP disputes. While not material currently, adverse outcomes could restrict product capabilities.

- Small-cap liquidity: Only 115 employees, $1.15B market cap, 1.1M average daily volume. Institutional ownership is limited, creating both risk (volatility) and opportunity (re-rating potential as institutions discover the name).

Investment Thesis

Why Buy at $40

- Monopoly at the trough: The stock is at peak negative sentiment (Q2 revenue miss, SiC weakness, margin compression) — but the AI order cycle is confirmed and accelerating.

- $14M order de-risks the thesis: This is not a hope trade. Production orders from a named AI processor customer, shipping within 6 months, confirm demand is real and converting.

- Consensus is 50–100% too low: $76.3 FY27E assumes moderate ramp. $60–80M in H2 bookings alone could drive FY27 revenue to $120–150M.

- Balance sheet supports the wait: Zero debt, $24.5 cash, no dilution risk. The company can fund operations through the trough without raising capital.

- $1B TAM is credible, not aspirational: AI processors ($350M), silicon photonics ($200M), SiC/GaN ($200M), memory ($150M) — each segment has named customers and confirmed orders.

- Multiple expansion ahead: As AEHR transitions from “SiC cyclical” to “AI infrastructure equipment,” the market will re-rate from 10–12x revenue (equipment cyclical) to 15–20x revenue (AI monopoly). This alone drives 50–100% upside even at current revenue levels.

Price Target: $60–$75

Based on FY27E revenue of $120–150M (above consensus) at 15x revenue multiple, the stock should trade to $60–$75 within 12–18 months. If the full TAM thesis plays out (AI + SiPho + Memory + SiC), $100+ is achievable by FY28.

What Would Change This View?

- H2 bookings come in below $40M (significant miss vs. $60–80M target)

- Lead AI customer cancels or delays orders

- A competitor demonstrates comparable wafer-level burn-in capability

- Hyperscaler capex budgets are cut 20%+ from current plans