What Is Photonics and Why Should Anyone Care?

Photonics is the science of using light instead of electricity to move data. Think of it this way: inside every data center that powers ChatGPT, Google Search, or Netflix, thousands of computer chips need to talk to each other. Right now, most of that “talking” happens through tiny copper wires but copper is running out of steam. It cannot move data fast enough, and it generates too much heat.

Photonics replaces those copper wires with laser beams traveling through glass fibers. Light moves faster, carries more data, and uses less electricity. That’s why every major tech company Google, NVIDIA, Microsoft, Meta, Amazon is now spending billions to switch from copper to light.

This is not a future technology. It’s happening right now, and it is creating one of the fastest-growing markets in the semiconductor industry.

The Money Trail: Follow the Spending

Big Tech is spending nearly $700 billion on AI in 2026

The five largest tech companies Amazon, Google, Microsoft, Meta, and Oracle have collectively committed to spending between $660 billion and $690 billion on data center infrastructure in 2026. That’s nearly double what they spent in 2025. To put this in perspective, that is more than the entire GDP of Switzerland spent in a single year on computer buildings.

About 75% of that spending, roughly $450 billion goes directly to AI infrastructure: GPU chips, AI servers, and the data centers that house them. The remaining 25% covers traditional cloud, networking, real estate, and power systems.

A slice of that spending goes to photonics and it’s growing fast

Within the networking portion (~$50 billion), optical transceivers and photonic components represent a rapidly growing share. The global optical transceiver market was valued at $14.7 billion in 2025 and is projected to reach $46 billion by 2034, growing at 17% annually. But the AI-specific portion is growing much faster.

LightCounting, the leading industry research firm, estimates that the AI cluster optics market alone reached $16.5 billion in 2025 and will hit $26 billion in 2026 that’s 60% growth in a single year.

How Photonics Actually Works (The Simple Version)

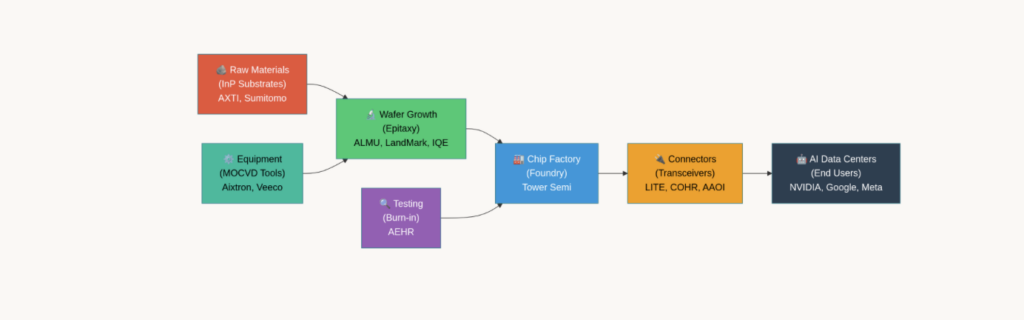

Imagine building a highway system. Photonics has a supply chain just like any highway does:

- Raw Materials (the ground): Special crystals called Indium Phosphide (InP) serve as the foundation. Think of them like the bedrock you build roads on. Only a few companies in the world make these crystals.

- Wafer Growth (laying the asphalt): Thin layers of semiconductor material are grown on top of those crystals, atom by atom. This is called epitaxy. These layers become the active part of the laser that generates light.

- Equipment (the construction machines): Specialized machines called MOCVD reactors are the “cranes and bulldozers” of photonics. Without them, no lasers get made.

- Testing (quality inspection): Before any chip ships, it must be stress-tested at extreme conditions to catch defects. One bad chip in a $500 million AI cluster can take down an entire rack.

- Chip Factory (foundry): The layers get processed into working laser chips and photonic circuits at a semiconductor factory.

- Connectors (the on-ramps): Finished laser chips get assembled into optical transceivers — small pluggable modules that convert electrical signals from a computer chip into light signals that travel through fiber.

- AI Data Centers (the drivers): NVIDIA, Google, Meta, and Microsoft buy these transceivers by the millions to connect their GPU clusters.

Why This Market Is Exploding Right Now

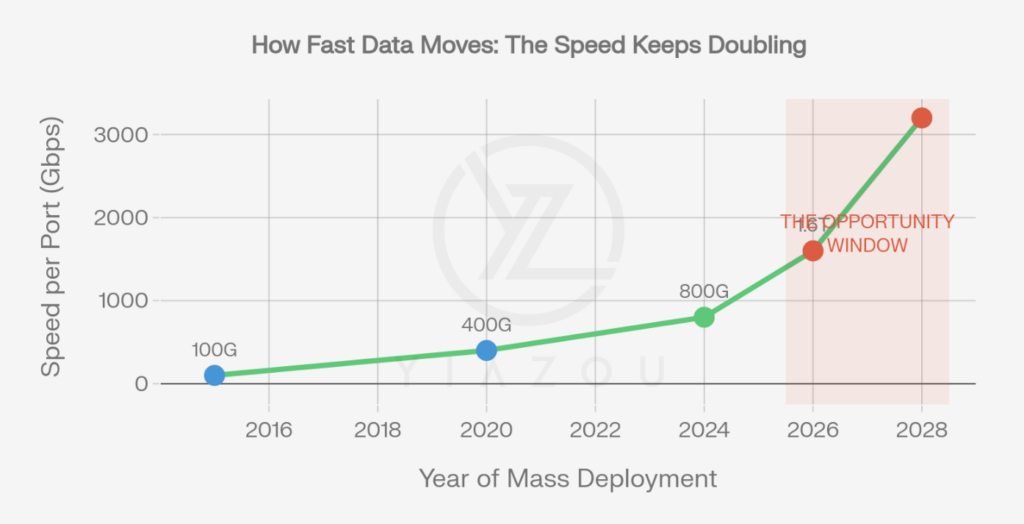

Data center connections have evolved from 100 Gbps (gigabits per second) in 2015 to 800 Gbps today, and are moving to 1,600 Gbps (1.6T) by 2026. Each speed generation requires entirely new laser chips, new transceivers, and new testing equipment. The industry is currently in the middle of the biggest speed transition ever from 400G to 800G with 1.6T already in the pipeline.

Shipments are growing at an extraordinary pace

Worldwide shipments of 800G and higher transceivers are expected to hit 24 million units in 2025 and then jump 2.6 times to 63 million units in 2026. That kind of growth from basically zero in 2023 to 63 million units in 3 years is almost unprecedented in the semiconductor industry.

AI Models Are Getting Bigger

AI training models now exceed 100 trillion parameters. Training a single model can require thousands of GPUs working together, and those GPUs need to share data continuously. The bigger the model, the more data needs to move between chips. Copper connections cannot handle this, creating a physical bottleneck that only photonics can solve.

As one industry expert put it: “The question is no longer whether optical interconnects will dominate data center architectures, but how quickly the ecosystem can mature”.

The Big Bottleneck: Not Enough Raw Materials

Here’s where it gets really interesting for investors. The entire photonics industry depends on a rare material called Indium Phosphide (InP) and there isn’t enough of it. Global demand for InP devices reached 2 million units in 2025, but production capacity was only 600,000 units a 70% supply gap. Orders at major InP suppliers are fully booked through 2026. Industry buyers are reportedly saying: “Price is not an issue. We just want to secure the quantities”.

This shortage exists because:

- Only 2–3 companies in the world make InP substrates at scale (AXT and Sumitomo control ~75% of supply).

- New factories take years to build, not months — and equipment lead times stretch 18–24 months.

- China controls a large share of production, and export permits are required, adding geopolitical risk.

- The bottleneck is so severe that NVIDIA has pre-allocated capacity at key laser suppliers, leading to extended lead times beyond 2027 and a worldwide shortage.

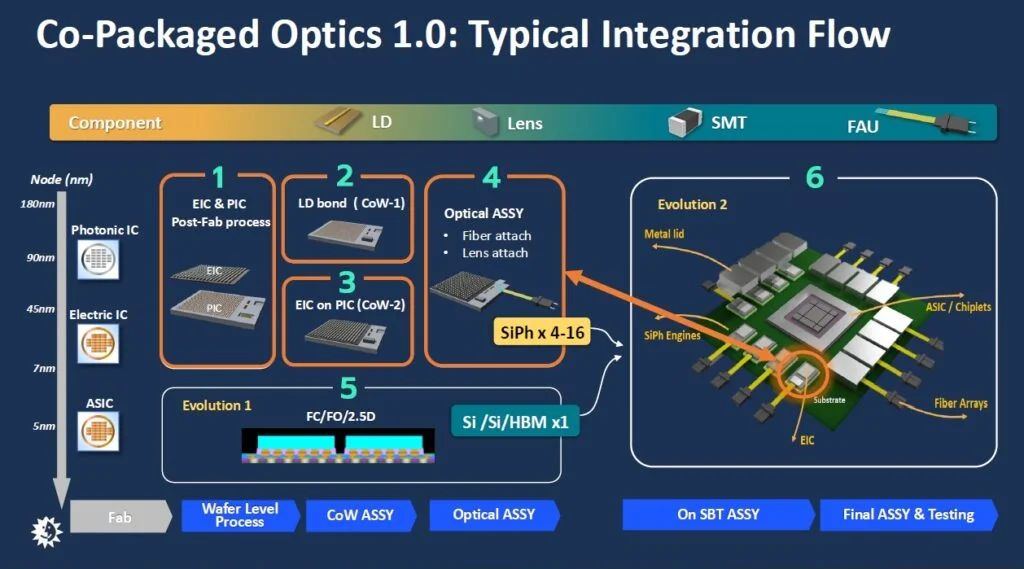

What Comes Next: Co-Packaged Optics

The current approach, plugging separate transceiver modules into the front of a network switch, works today. But the industry is already developing the next generation: Co-Packaged Optics (CPO), where lasers and light guides are built directly onto the chip itself.

CPO promises 70% power savings for AI workloads compared to traditional pluggable optics. Broadcom forecasts that CPO will reach the energy efficiency needed for mass deployment (below 10 picojoules per bit) by 2028, with advanced versions hitting 5 pJ/bit by 2029.

Large-scale CPO deployment is expected between 2028 and 2030. The CPO market is projected to exceed $20 billion by 2036, growing at 37% annually from 2026. This means the photonics opportunity doesn’t peak in 2027, it accelerates into the next decade.

The Investment Landscape

The market has already begun recognizing the photonics theme. Several stocks in the space have delivered extraordinary returns over the past year:

| Company | What They Do | 1-Year Return | Market Cap |

|---|---|---|---|

| AXTI | InP substrate crystals | +3,254% | $1.7B |

| LITE | Laser chips for transceivers | +864% | $50.0B |

| AEHR | Chip testing/burn-in | +297% | $1.1B |

| COHR | Lasers + silicon photonics | +222% | $41.1B |

| AAOI | 800G transceivers | +202% | $5.8B |

| TSEM | Photonics chip foundry | +191% | $14.0B |

| ALMU | Next-gen wafer growth | +143% | $219M |

| CRDO | High-speed connectors | +108% | $20.3B |

| MRVL | Custom AI chips/DSPs | +69% | $69.3B |

Where the market has already priced in the story

The big transceiver makers: Lumentum (LITE), Coherent (COHR), and Applied Optoelectronics (AAOI) have already seen massive rallies. LITE trades at 202x earnings, COHR at 251x, and AAOI at a negative P/E with a stock price 2x above analyst consensus targets. These companies are the most visible beneficiaries, but the stocks now reflect very high expectations.

Where the market has NOT yet priced in the story

The upstream supply chain the companies that make the raw materials, grow the wafers, build the equipment, and test the chips remains dramatically undervalued relative to the downstream transceiver makers. The reason is simple: most investors don’t know these companies exist.

| Layer | Example Company | Market Cap | Why It’s Interesting |

|---|---|---|---|

| Raw materials | AXT (AXTI) | $2B | 40% of global InP supply, but China export risk |

| Wafer growth | Aeluma (ALMU) | $280M | Solves InP shortage with new technology, DoD-backed |

| Equipment | Aixtron (AIXA) | $3B | Makes 90% of the machines all laser makers need |

| Testing | Aehr Test (AEHR) | $1.15B | Only company doing wafer-level burn-in for AI chips |

| Foundry | Tower Semi (TSEM) | $14B | NVIDIA’s silicon photonics manufacturing partner |

The Simple Investment Thesis:

The logic is straightforward:

- AI spending is accelerating: $690B in 2026, potentially $1.2 trillion by 2030.

- AI needs photonics: copper cannot handle the bandwidth, and models keep getting bigger.

- Photonics needs InP: there’s a 70% supply gap in the critical raw material.

- Supply takes years to build: new fabs take 2–3 years, equipment lead times are 18+ months.

- The transition to CPO extends the boom: large-scale CPO deployment in 2028–2030 means photonics demand grows for years, not quarters.

The companies that control the chokepoints in this supply chain the ones that make the crystals, grow the wafers, build the machines, and test the chips stand to benefit disproportionately. Many of them are small companies (under $2B market cap) in an industry where the end customers (NVIDIA, Google) are worth trillions.

Key Risks to Watch:

No investment thesis is without risks. The major concerns for photonics:

- AI spending slowdown: If hyperscalers cut capital budgets (as they did in 2022–23), photonics demand drops sharply. LightCounting warns that “any slowdown in purchases by Nvidia or Cloud companies can reverse the market dynamics, piling up excess inventories”.

- Silicon photonics disruption: If silicon-based solutions replace InP lasers faster than expected, pure InP companies lose their advantage. This is a 3–5 year risk, not immediate.

- China/geopolitics: A significant share of InP production occurs in China. Export permit delays have already caused quarterly revenue misses at AXT. Escalating trade restrictions could disrupt the entire supply chain.

- Concentration risk: NVIDIA has locked up capacity at key laser suppliers. If NVIDIA’s roadmap shifts (e.g., away from pluggable optics toward CPO faster), some transceiver makers could see demand evaporate quickly.

- Valuation risk: Many photonics stocks have already tripled or more. A broad market correction could hit these high-multiple names disproportionately.

Takeaway

The numbers tell a clear story: photonics is transitioning from a niche telecom market into a core AI infrastructure market. The AI cluster portion alone ($26B in 2026) is growing faster than the total traditional optical market did in a decade. This demand is structural driven by physics (copper limitations) and economics (AI training costs), not cyclical.