Aeluma (ALMU) is best understood as an early-stage, R&D-heavy compound-semiconductor/photonics platform rather than a near-term “volume optics” story. Its core ambition is to bring high-performance III–V materials (e.g., InGaAs for SWIR sensing, quantum-dot gain media for lasers) onto large-diameter, CMOS-compatible substrate so that “exotic” photonics can ride the manufacturing economies of scale of mainstream silicon.

The company’s commercial proof points are still emerging, but its credibility is anchored by multiple U.S. government-funded programmes, including an DARPA contract of $11.7M with milestone-gated funding and defined subcontractor roles (including Teledyne Scientific Company and University of California, Santa Barbara). Its broader government set includes work with NASA, the U.S. Navy, the U.S. Department of Energy, and the Office of the Secretary of Defense largely aligned with quantum photonics, harsh-environment sensing, and advanced interconnects.

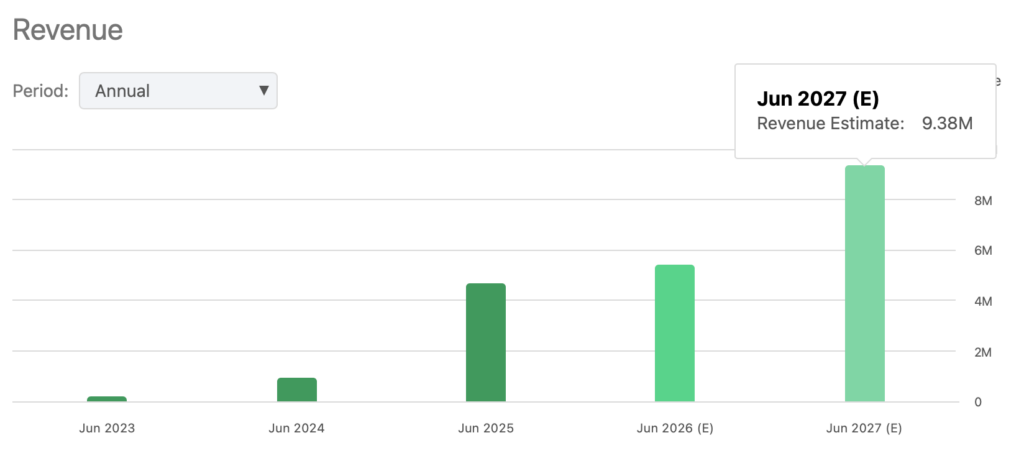

At today’s valuation, the market is already pricing in a non-trivial probability that Aeluma’s heterogeneous integration transitions from contracts and prototypes to repeatable commercial design wins. With a share price of $16 and ~18.05M shares outstanding, market cap is ~US$260M; cash is ~US$38.6m, with no traditional long-term debt—so EV is still ~US$223M. On trailing revenue (TTM ≈ $5.23m, calculated from SEC-reported half-year revenues), that implies a venture-style revenue multiple (~40x) and a valuation that leaves limited room for execution stumbles.

Business Model & Strategic Positioning

Aeluma makes money today in two main ways: small product/service contracts and government-funded projects. Most of its current revenue comes from milestone-based government contracts, meaning it gets paid as it completes specific technical steps. So far, its customers are mainly government agencies, not large commercial buyers placing repeat production orders.

In the near term, Aeluma is focused on three product areas:

- SWIR detectors for sensing and imaging,

- High-speed photodiodes for optical communications, and

- Quantum-dot lasers aimed at data center and telecom interconnects.

Longer term, it wants to integrate these quantum-dot lasers directly into silicon photonics platforms and expand into quantum and nano-scale semiconductor applications.

Manufacturing is designed to stay lean. Aeluma handles prototyping and small batches in-house at its cleanroom facility in Goleta, California, but relies mostly on external foundries to scale production. Management recently emphasized improving wafer quality, performance, and yield with foundry partners, which is critical if this ever moves beyond lab demonstrations into real manufacturing.

The company is also working with industry and research partners, including AIM Photonics, RFSUNY, and Thorlabs Crystalline Materials, to advance integration of lasers and nonlinear materials onto silicon platforms. In simple terms, Aeluma isn’t trying to compete with today’s large optics manufacturers. It’s trying to position itself as a technology layer that could sit inside future AI, quantum, and sensing hardware systems, if its integration approach proves scalable.

What “Heterogeneous Integration” Means

Think of silicon as the world’s best factory material. It’s cheap at scale, extremely repeatable, and the entire CMOS ecosystem (the stuff behind modern electronics) is built around it. The catch? Silicon is great at guiding light around (passive photonics) but it’s lousy at making light.

That’s where III–V materials (like InGaAs and other compound semiconductors) come in. They’re excellent at active optoelectronics: lasers, high-sensitivity photodetectors, nonlinear optical effects. “Heterogeneous integration” basically means: let’s marry silicon’s manufacturing scale with III–V performance, in a way that can be produced with high yields, not just shown once in a paper.

Why It Matters Now?

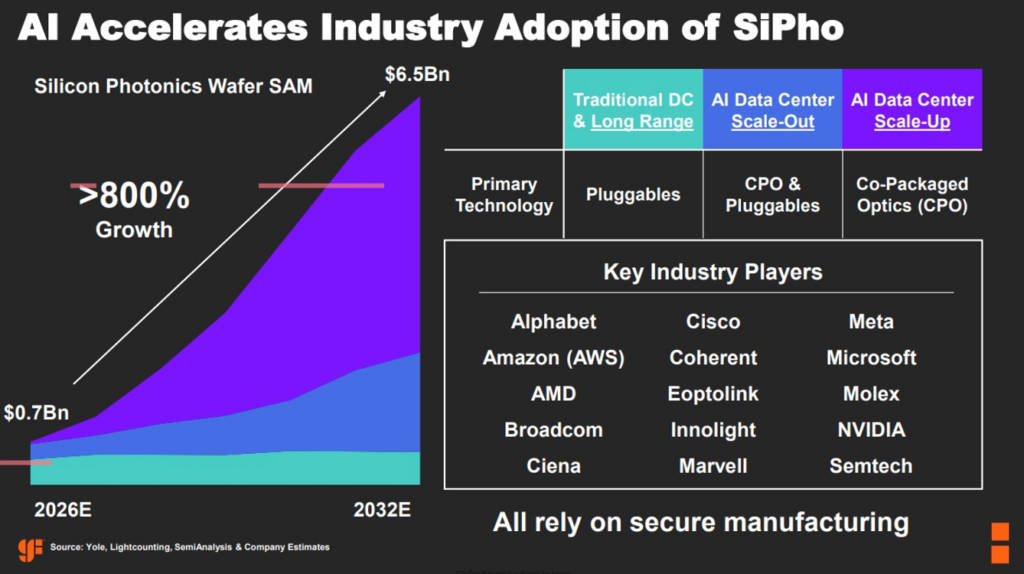

As traditional transistor shrinking slows down, the bottleneck shifts to moving data, inside a data center, inside a server, even inside the package. Power and bandwidth become the limiter. So industry roadmaps increasingly point to photonics + electronics co-integration and advanced packaging (including co-packaged optics) as the next lever.

In plain English: instead of pushing electrons through copper traces at insane speeds (hot, power-hungry), you increasingly want light-based interconnects, but that only works if you can integrate the light sources and detectors into practical, manufacturable systems.

The “Hard Problem”: Lasers on Silicon

Routing light on silicon? Easy-ish. Creating an on-chip laser on silicon? That’s the pain point. Practical lasers usually need III–V “gain” material. But growing or attaching III–V onto silicon creates ugly physics and manufacturing headaches: crystal defects from lattice mismatch, stress from thermal mismatch, yield losses from bonding/transfer, and CMOS process constraints (temperature budgets and contamination rules).

Even if a device works in a prototype, mass adoption typically requires long reliability tests, packaging validation, and stable process control. That’s where many “cool demos” quietly stall.

Why Quantum Dots Get Hype

Quantum-dot lasers are a big deal because they tend to be more tolerant of defects and more stable across temperature swings than older structures (like quantum wells). That matters because silicon integration is basically an imperfect marriage, you’re trying to make materials coexist that don’t naturally want to.

So quantum dots are one of the more realistic routes to “good-enough” lasers that can survive real-world manufacturing and deployment.

The Moat Is Process

Aeluma’s roadmap lines up with two active battlegrounds:

1) InGaAs for SWIR sensing (detectors/APD/SPAD paths). SWIR sensors are powerful, but traditionally expensive and tied to smaller wafers. The pitch is that moving toward larger-diameter, silicon-compatible manufacturing could unlock scale economics—though dark current, noise, packaging, and reliability are still the gatekeepers.

2) Quantum-dot lasers for silicon photonics, targeting WDM and co-packaged optics architectures. The field shows progress—even on 300mm wafer directions—but turning that into high-yield production is the real fight.

So the “moat” isn’t one flashy device screenshot. It’s whether Aeluma can turn integration into a repeatable, foundry-compatible process flow that customers actually qualify and adopt. Patents and know-how help, sure—but the true scoreboard is qualification-stage pull-through, not Phase-2 “we’re evaluating” language.

Where Aeluma’s Real Test Begins

Aeluma’s customer pipeline is helpful, but it also keeps expectations grounded. Their typical path runs from early discovery to evaluation, then to initial paid development work, and eventually to qualification, where a customer formally locks in the design and approves the production process. Only after qualification do you get repeatable, scalable production orders. Right now, most of Aeluma’s reported engagements sit in the middle stages. That signals interest, not guaranteed commercial traction.

The real value inflection happens at qualification. That’s when the technology moves from “promising” to “production-ready.” Until then, revenue is largely milestone-based R&D funding. In semiconductor and photonics platforms, especially when new materials are involved, it often takes multiple years to transition from lab success to reliable, high-yield manufacturing. The gating factors are usually yield improvement, long-term reliability testing, packaging validation, and supply-chain readiness.

So the pipeline shows momentum, but not inevitability. The key question isn’t how many engagements exist, it’s how many advance into qualification and then into repeat production. That transition is what ultimately determines whether Aeluma becomes a scalable commercial platform or remains primarily an R&D-focused player.

Contracts & Commercialisation Mechanics

The contract portfolio is not just “validation”; it also defines how revenue tends to appear: milestone-based and lumpy, often tied to deliverables rather than recurring shipments. The company’s SEC disclosures explain that government contracts may be cost-reimbursement or fixed-price and that payments can be made upon completion of specified milestones, with revenue recognised upon achieving designated milestones (or over time, depending on contract structure).

A key datapoint: for FY2025 the company reported it was awarded six government contracts totalling $13.8M, and it ended FY2025 with $10.2M of remaining performance obligations under obligated government contracts. By Dec 31, 2025, remaining performance obligations under obligated government contracts were $7.9M, reflecting both revenue recognition and the pace of new awards.

Key Disclosed Awards:

| Award / programme | Date received / announced | Max value disclosed | Technical focus (as disclosed) | Noted partners / structure |

|---|---|---|---|---|

| DARPA heterogeneous integration (M‑STUDIO) | Received Sep 2024 (SEC) / referenced in filings | $11.7m | HI for nano-scale semiconductors compatible with leading-edge advanced nodes; apps include AI, mobile, 5G/6G | Milestone-gated: ~$6.0m expected invoiced first 18 months + ~$5.7m next 18 months (SEC); subcontractor roles disclosed in offering doc (Teledyne Scientific + UCSB). |

| NASA quantum-dot photonic ICs on silicon | Received Aug 2024 (SEC) / announced Nov 2024 | Not disclosed | Quantum-dot PICs on silicon for space/aerospace; also positioned for AI/HPC interconnect | NASA collaboration (press); amount not disclosed in cited materials. |

| DOE SWIR photodetectors | Received Apr 2025 (SEC) / announced Apr 2025 | Not disclosed | Low-cost SWIR photodetectors; commercialisation-oriented sensing roadmap | DOE press release; amount not disclosed in cited materials. |

| U.S. Navy high-speed photodetectors | Received Jun 2025 / announced Jun 2025 | Up to $1.3m | High-speed photodetectors for optical interconnects; government + commercial relevance | Disclosed inclusion of a “major global interconnect manufacturer” as proposed subcontractor plus prime-contractor support. |

| U.S. Navy low-SWaP imaging sensors | Received Jun 2025 / announced Jul 2025 | Not disclosed | Low-SWaP imaging sensors for next-gen submarine systems; VIS+SWIR multi-spectrum in a compact chip | Amount not disclosed; aligns directly with SWIR-on-silicon thesis. |

| NASA entangled photon sources / quantum photonics scaling | Received Sep 2025 (SEC) / announced Jul 2025 | Not disclosed | Commercialise entangled photon sources; integrates nonlinear optical materials on CMOS-standard 200mm silicon | Demo references wafer-scale nonlinear materials integration; external reporting cites collaboration with Thorlabs Crystalline Materials. |

| OSD single-photon avalanche detectors | Announced May 2024 | Not disclosed | SPADs for satellite and lunar ranging | Amount not disclosed in press release. |

| RFSUNY contract funding (AIM Photonics 300mm laser integration) | Mentioned Feb 2026 | Not disclosed | Quantum-dot laser integration into AIM Photonics 300mm silicon photonics platform | Reported in Feb 2026 earnings release; amount not disclosed. |

Sources: SEC filings and company releases/earnings materials.

What This Implies for Commercialisation Quality

Revenue today appears heavily weighted to government-funded R&D and milestone billing—not a stable, high-visibility product shipment stream. In the Feb 2026 10‑Q, the company disclosed that all customers were government agencies and that revenue and receivables were concentrated among a small number of customers. That matters for “structural bet” investors because government contracts can validate technical relevance while still leaving commercial adoption risk largely unresolved.

Cash-Rich, Revenue-Light: The Real Execution Test

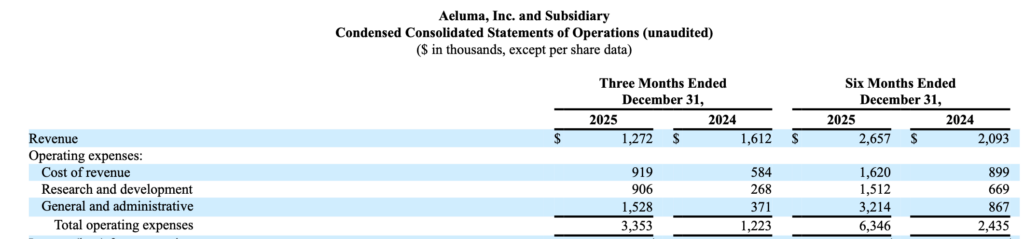

For the six months ended Dec 31, 2025, revenue was $2.657M versus $2.093M in the prior-year period, while operating expenses were $6.346M, producing a six‑month GAAP net loss of $3.346m. The quarter ended Dec 31, 2025 had revenue of $1.272M and GAAP net loss of $1.853M, with higher R&D and G&A reflecting hiring and build-out. For FY2025, revenue was $4.665M and GAAP net loss was $3.022M.

Cash is strong relative to the revenue base: at Dec 31, 2025, cash and cash equivalents were $38.572M, total assets $42.57M, and total liabilities $1.767M (primarily lease liabilities), with shareholders’ equity $40.803M. Current assets of $40.263M versus current liabilities of $0.825M imply an unusually high current ratio (~48.8x), reflecting overcapitalisation relative to current operating scale.

Runway Scenarios & Sensitivity

In the first half of FY2026, net cash used in operations was ~$1.1M, with modest investing outflow; annualising that would imply a very long cash runway, but it is unlikely to remain stable if commercialisation efforts and manufacturing readiness spend accelerate.

The charts below frame the tension: the balance sheet can fund multiple years of execution, yet a real scale-up (qualification, packaging, test, supply-chain build-out) can compress runway meaningfully without additional capital, especially given the company’s shelf registration capacity and history of equity raises.

A revenue-path sensitivity (illustrative; $m) highlights what would need to go right for today’s multiple to “grow into itself”:

| FY revenue ($m) | 2026 | 2027 | 2028 | 2029 |

|---|---|---|---|---|

| Bear | 4 | 5 | 8 | 12 |

| Base | 5 | 10 | 25 | 50 |

| Bull | 6 | 20 | 50 | 100 |

Assumptions: FY2026 is anchored to company guidance; later years reflect plausible ranges for (i) continued contract/NRE layering with slow product ramp (bear), (ii) initial commercial design wins and qualification-led growth (base), and (iii) successful platform adoption into interconnect and sensing niches with accelerating volume (bull).

At the current ~$260M market cap, implied P/S would still be ~52x even on $5M revenue (base FY2026) and only falls into more conventional territory if revenue reaches multi‑tens of millions.

Why ALMU Is Different From Other Players

The simplest answer to “why ALMU and not AAOI/LITE?” is that you are not buying the same thing. AAOI and LITE are primarily operating photonics component suppliers with established (though cyclical) commercial demand and margin structures; ALMU is a platform R&D-to-productisation bet where most revenue is still milestone/NRE/contract-shaped, and valuation is dominated by long-dated optionality on a manufacturing breakthrough.

Interpretation

- ALMU vs AAOI/LITE: AAOI and LITE may benefit from the same macro tailwind (AI networking and bandwidth growth), but they are not pure HI “process platform” bets; they are businesses with customer purchase orders, manufacturing scale, and competition on cost/roadmaps. ALMU, by contrast, is closer to a public-market analogue of a venture investment in manufacturing IP—where the payoff is nonlinear if (and only if) qualification and adoption happen.

- ALMU and POET are both AI photonics plays, but they sit at different layers. ALMU is an upstream materials and process bet, focused on integrating III–V materials onto silicon for future AI, quantum, and defense hardware. It’s R&D-driven and dependent on qualification and foundry adoption. POET is a downstream product play, developing optical engines for AI data centers with early production orders targeting 800G/1.6T markets. ALMU is a long-dated architecture optionality bet. POET is a nearer-term commercialization bet tied directly to AI networking demand. Different timeline. Different risk curve. Different execution hurdles.

- Why the multiple is so high: The market is effectively paying upfront for the possibility that Aeluma becomes an enabling technology layer inside future silicon photonics and sensing supply chains (including co-packaged optics architectures), not for its current revenue stream.

- A useful mental model: If you want exposure to AI optics now, AAOI/LITE/COHR are nearer to the demand signal. If you want exposure to “the next integration paradigm” (III–V-on-silicon at scale), ALMU is more intellectually aligned, but much riskier and far less de-risked commercially.

Takeaway

ALMU has real technical interest and a growing engagement pipeline, but the true inflection depends on customers advancing into qualification and repeat production. Until that happens, revenue remains R&D-driven. The opportunity is meaningful but commercial scale, not engagement count, will determine whether the thesis truly materializes.