Analyst Recommendation: BUY

Rating: ★★★★☆ (4/5 stars)

INVESTMENT THESIS:

1. Dominant Technology Position with Limited Competition

Kraken Robotics (KRKNF/PNG.V) controls the industry-leading Synthetic Aperture Sonar (SAS) technology and proprietary SeaPower pressure-tolerant battery platform, creating significant barriers to entry. The company’s 3 cm * 3 cm resolution at 200m range is among the highest in the industry, while SeaPower batteries deliver roughly twice the energy density and lower lifecycle cost than conventional oil-filled alternatives. This technological moat is reinforced by integration into 20+ UUV platforms globally and NATO adoption across 20+ countries.

2. Explosive Anduril Partnership Scaling Opportunity

The partnership with Anduril Industries ($30B valuation, Palmer Luckey-founded) represents a multi-billion-dollar revenue opportunity. Kraken supplies $2-10M of technology per Ghost Shark XL-AUV and DiveLD platform. With Australia’s $1.7B Program of Record announced September 2025 for “dozens” of Ghost Sharks (deliveries starting January 2026), Anduril’s Rhode Island facility is designed for production of more than 200 Dive-LD units per year at full capacity, and additional orders from US Navy (Replicator program), Japan, South Korea, and allied nations, the partnership could generate $200-400M CAD annually by 2027, exceeding Kraken’s total current revenue in a single relationship.

3. Inflection to Profitability with Recurring Revenue Streams

Kraken has transitioned from loss-making R&D (2020–2022) to roughly 17 – 18 % normalized net margins in 2024, reflecting its first sustained profitability. To meet its CAD $120–135 million revenue target, Kraken must nearly double H1 output in H2 2025, making guidance ambitious.

Service revenue (recurring, high-margin RaaS model) is growing 47% YoY, diversifying away from lumpy project-based hardware sales. New factory capacity and battery expansion provide operating leverage for 30%+ CAGR through 2027.

COMPANY OVERVIEW:

Corporate Structure

Legal Entity: Kraken Robotics Inc., incorporated in Newfoundland and Labrador, Canada

Headquarters: St. John’s, Newfoundland and Labrador, with operations in Boston, Sydney, Galway, and Delf

Listings:

- TSX Venture Exchange (TSXV): Ticker symbol: PNG

- OTCQB (US): Ticker symbol: KRKNF

- Stuttgart Stock Exchange: Ticker symbol: 2KQ:STU.

- Hamburg Stock Exchange: Ticker symbol: 2KQ:HAM.

Fiscal Year End: December 31

Exchange Rates (Reporting): CAD/USD average ~0.75 for 2024; all financial statements filed in CAD

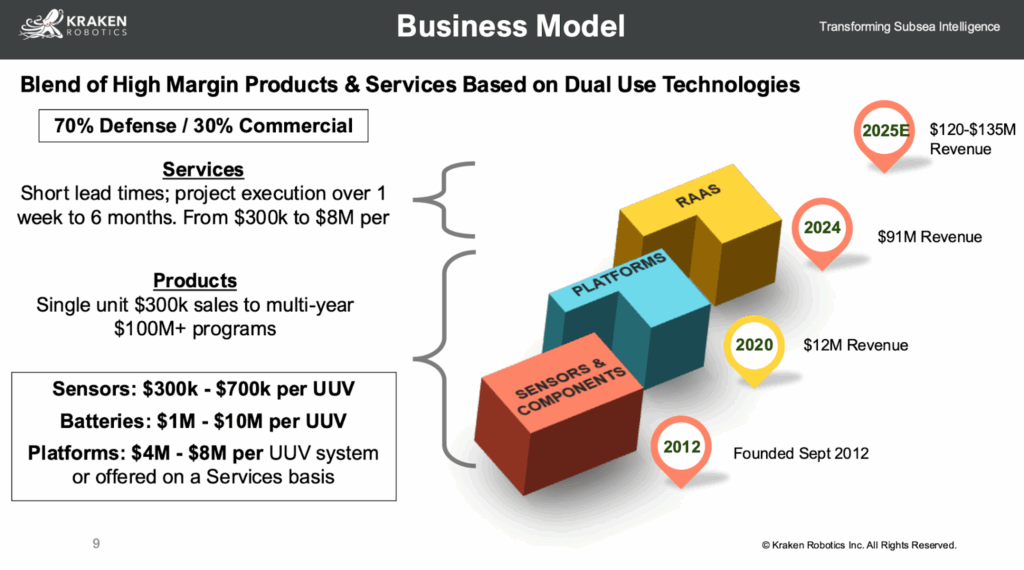

Business Model

Kraken operates as a subsea intelligence and autonomy company with three primary revenue streams:

- Product Sales (72% of 2024 revenue, ~CAD $66.3M)

- Synthetic Aperture Sonar systems ($2-5M per unit)

- SeaPower batteries ($1-10M per contract depending on scale)

- Support hardware and integration services

- Service Revenue (28% of 2024 revenue, ~CAD $25M)

- Robotics-as-a-Service (RaaS): sub-bottom imaging, acoustic coring, LiDAR surveys

- Field support for deployed platforms

- Post-mission analysis consulting

- Acquisition-Driven Growth

- 3D at Depth Inc. (August 2025): US ITAR-compliant subsea LiDAR and services

- Provides direct US market access, DoD relationships, GSA schedule

History & Key Milestones

- 2017: Genesis with 3D at Depth as separate company (acquired 2025)

- 2018-2019: Kraken Sonar Inc. formation; early SAS development

- 2020: Public listing on TSX-V; revenue CAD $12.3M, net loss ($5.2M)

- 2021-2022: SAS product development; battery program genesis

- 2023: Profitability achieved; $69.6M revenue (+70% YoY); EBITDA $11.7M

- 2024: Scale inflection; $91.3M revenue (+31% YoY); net income $20.1M; EBITDA $18.1M

- April 2025: Q1 earnings reaffirm FY guidance; assets jump to $178.8M

- August 2025: Q2 2025 revenue rose 13% sequentially from Q1 but declined 3% year-over-year for the first half.

- August 2025: CAD $115M bought-deal equity raise (30% share dilution)

- September 2025: Announce $13M in new orders (US, Norway, Turkey); Anduril Ghost Shark Program of Record awarded (AUD $1.7B / USD $1.12B)

- October 30, 2025: Anduril opens Ghost Shark manufacturing facility; first unit rolls off ahead of schedule

The Strategic Context: When Power Moves Under the Ocean

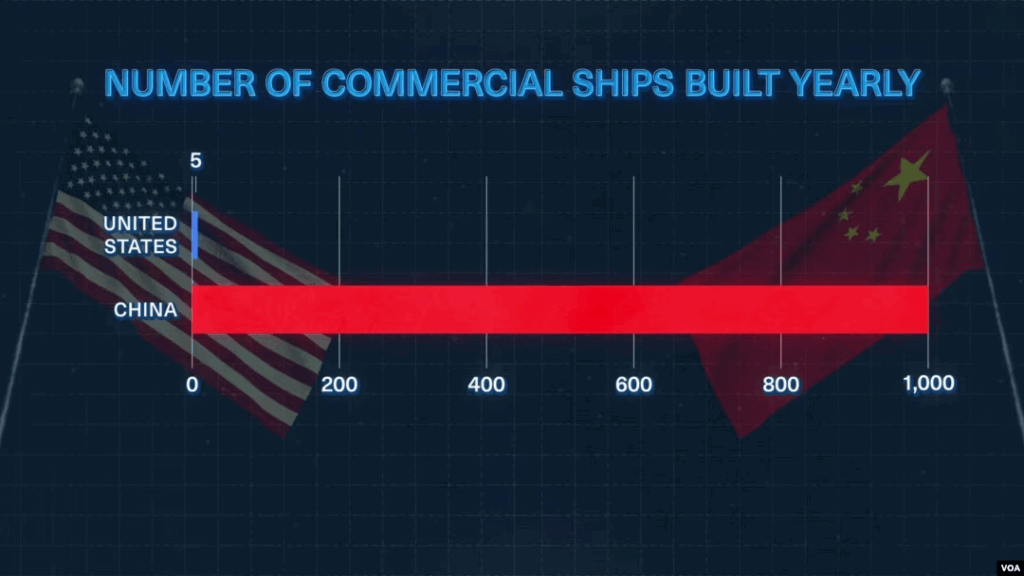

In the evolving theater of global defense, dominance no longer belongs solely to those who control the air or cyberspace. The next great frontier is unfolding beneath the waves. The Wall Street Journal recently warned that China is on the verge of becoming a world-class submarine power, deploying fleets that are quieter, deeper, and faster, equipped with sensors that can track adversaries with unprecedented precision. Beijing’s navy is rapidly modernizing, and its ambitions extend deep into the Pacific, including drills around Taiwan and aggressive posturing across key maritime choke points.

For the United States and its allies, this escalation is a wake-up call. Roughly 60% of America’s submarine force is already stationed in the Indo-Pacific, yet the Pentagon’s own defense planners have acknowledged the growing asymmetry of industrial capacity. China now out-builds the United States by more than 200 to 1 in shipbuilding tonnage. To maintain deterrence, the United States must compensate not by matching volume but through exponential technological leverage, through autonomy, data, and networked systems capable of operating invisibly beneath the surface.

This is precisely the niche that Kraken Robotics occupies. The company has become one of the most important, if still underappreciated, suppliers of critical subsea technologies. Its synthetic aperture sonar systems, pressure-neutral batteries, and LiDAR-based imaging solutions are forming the sensory and power backbone of the emerging underwater defense network. While the world’s attention remains fixed on AI chips and aerial drones, Kraken is quietly building the infrastructure that will define the coming decade of underwater autonomy.

Kraken’s Mission: Bringing Vision, Power, and Intelligence to the Deep

Kraken Robotics, headquartered in Newfoundland, Canada, operates on a deceptively simple premise: to make the invisible ocean visible, and to give the world’s underwater robots the energy and data intelligence to function autonomously for long durations at crushing depths. The company’s products fall into three core categories that together form a vertically integrated technology stack.

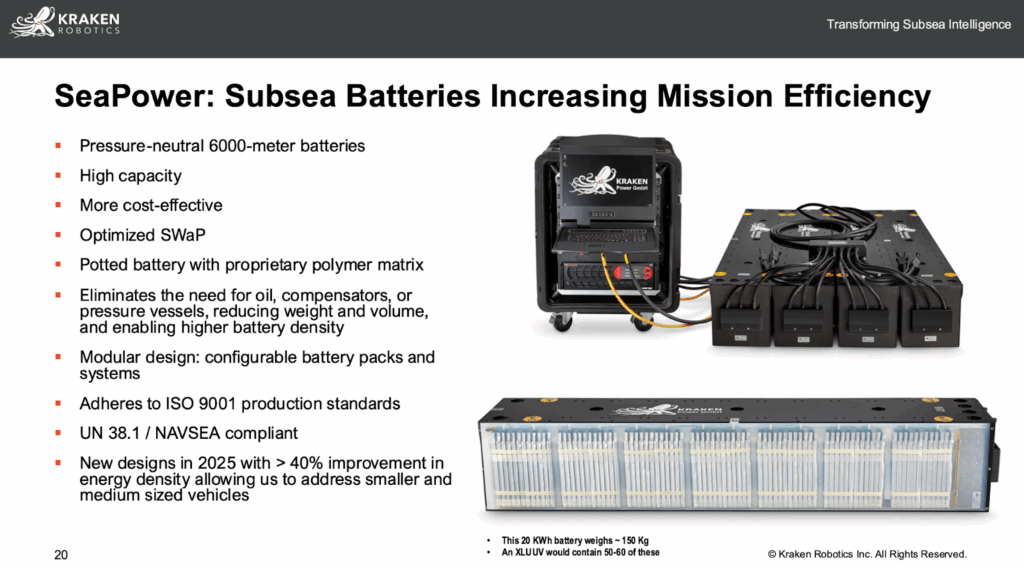

The first pillar is its SeaPower subsea battery platform, designed for use at depths of up to 6,000 meters. These batteries use a proprietary polymer encapsulation method that eliminates the need for bulky oil-filled pressure vessels. The result is a system with two to three times greater energy density and nearly half the weight of conventional underwater batteries.

For unmanned underwater vehicles, known as UUVs, this translates directly into endurance, range, and stealth. The longer a submersible can remain below the surface, the safer and more effective it becomes. In operational terms, Kraken’s technology allows these craft to patrol for days without surfacing, dramatically expanding mission profiles for surveillance, mine countermeasures, and infrastructure inspection.

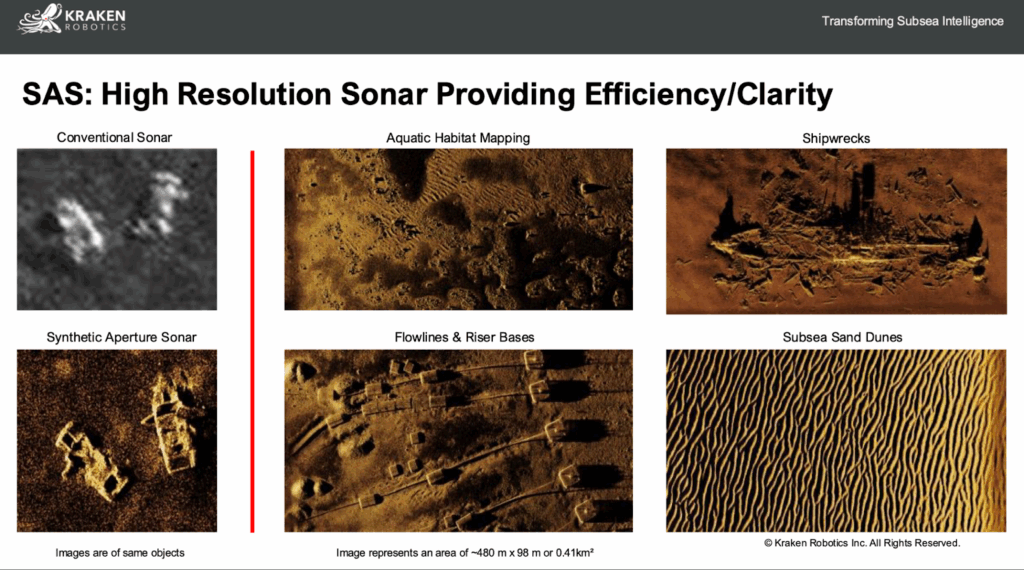

The second pillar is synthetic aperture sonar (SAS), Kraken’s original breakthrough. SAS technology fuses multiple acoustic pings into a coherent, high-resolution image of the ocean floor, providing centimeter-level accuracy at ranges exceeding 200 meters per side. Where traditional sonar produces grainy outlines, Kraken’s systems generate photographic-quality maps that can reveal objects as small as a soda can or a five-centimeter subsea cable. This has made the company’s sonar a favorite of NATO navies and commercial operators alike for tasks ranging from mine detection to pipeline monitoring.

The third pillar came through the 2025 integration of 3D at Depth, a LiDAR and analytics company acquired for roughly $17 million. The acquisition extended Kraken’s reach from two-dimensional acoustic imaging to three-dimensional laser scanning, allowing clients to build digital twins of their subsea assets. With gross margins above 60% and durable service revenues, 3D at Depth brought not only technology but recurring cash flow. It also positioned Kraken to expand its offerings beyond defense into offshore energy, renewables, and nuclear infrastructure inspection.

Individually, each business unit is valuable. Together, they give Kraken control over the full sensory and power chain of the underwater domain, a level of vertical integration rare among small defense suppliers and one that directly supports the strategic shift toward autonomous naval systems.

The Anduril Connection: From Supplier to Strategic Partner

The single most important development for Kraken’s future is its expanding partnership with Anduril Industries, the US defense technology company founded by Palmer Luckey and valued at more than $30 billion in its most recent private funding round.

In 2022 Anduril acquired Dive Technologies, a Massachusetts-based manufacturer of large unmanned submarines. Dive had already standardized on Kraken’s batteries and sonar systems. Rather than attempt to reinvent the wheel, Anduril deepened the partnership, making Kraken the de facto power and sensory provider for its entire underwater portfolio.

That portfolio now includes several classes of vehicles: the Dive-LD, a pickup-sized UUV for multi-day missions; the Dive-XL, also known as the Ghost Shark, a bus-sized platform capable of long-range surveillance and strike; and the Copperhead, a battery-powered smart torpedo that offers a fraction of the cost and deployability of traditional munitions.

Each of these relies heavily on Kraken’s technology. Estimates suggest that each Dive-LD carries roughly $1–2 million of Kraken hardware, while a single Ghost Shark may include as much as $8–10 million. Even the smaller Copperhead drones use between $100,000 and $250,000 of Kraken content per unit.

Anduril’s new 100,000-square-foot Rhode Island maritime facility is designed for production of more than 200 Dive-LD subsea drones per year at full capacity, in addition to the larger Ghost Shark and other vehicles. If Anduril ramps operations toward that scale, Kraken’s annual revenue contribution from this partnership could reach CAD $200–400 million under full-capacity and multi-program scenarios, roughly two to three times its 2024 revenue base. The synergy is significant: Anduril secures a proven, NATO-qualified supplier that shortens time-to-deployment, while Kraken gains leverage to one of the world’s fastest-scaling defense manufacturers.

Just as critical is the durability of this supply relationship. Substituting a certified component in defense procurement is a multi-year process requiring extensive requalification. Kraken’s SeaPower batteries are the only commercially proven pressure-neutral systems rated for 6,000 meters and qualified to U.S. Navy-level safety standards, using materials sourced outside China. Any competitor would face an 18- to 24-month qualification cycle at minimum. With the US Navy’s Replicator program aiming for full readiness by 2027, Anduril simply does not have that time. The result is a quasi-monopoly position for Kraken inside Anduril’s subsea bill of materials, at least for this procurement cycle.

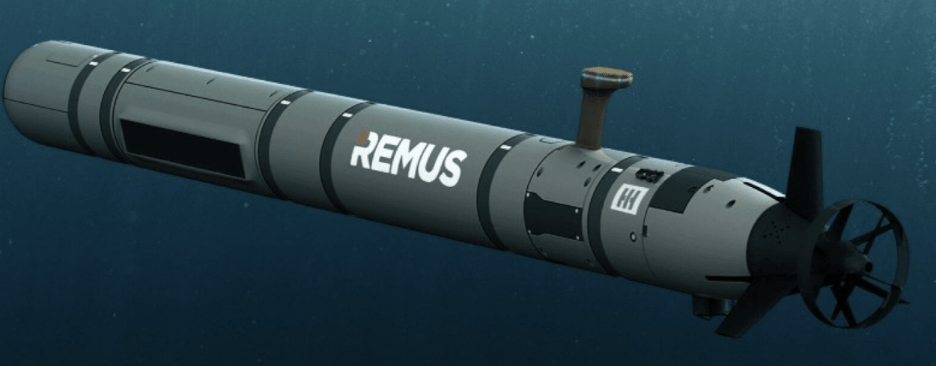

Beyond Anduril, Kraken’s technology is also used in HII’s REMUS underwater vehicles and has drawn interest from Boeing, General Dynamics, Kongsberg, and Saab, all of which are developing their own classes of unmanned submersibles. As UUV procurement moves from research budgets to production budgets, Kraken’s installed base gives it an inside track to win additional contracts.

The Moat: Operational, Not Theoretical

Kraken’s competitive advantage is not protected by a single patent or piece of code. It is built instead on operational readiness, certification, and embeddedness in customer programs.

Developing hardware that can survive 2,500 pounds per square inch of pressure at 6,000 feet, operate without failure for weeks, and integrate seamlessly into classified defense systems is no trivial feat. The technical barriers, combined with regulatory and security clearances, form an effective moat. Once a system passes qualification and is field-tested, military customers almost never switch suppliers.

Kraken’s lead in subsea batteries illustrates this perfectly. Battery manufacturers chasing electric vehicle markets are ill-equipped to design products for high-pressure, salt-corrosive environments. The few niche players that have tried to replicate Kraken’s polymer encapsulation process have failed to achieve the same energy density or safety standards. As a result, Kraken enjoys both technical leadership and institutional lock-in.

Even in sonar, where competition from Northrop Grumman’s Micro-SAS exists, Kraken retains an edge through focus and cost efficiency. It can deliver equivalent performance at roughly half the price while sustaining gross margins above fifty percent. That price-performance differential has made it the preferred choice for navies seeking rapid deployment over bureaucratic procurement cycles.

FINANCIAL OVERVIEW:

Financially, Kraken has executed one of the most remarkable transformations in the small-cap defense universe. In 2020 the company generated just $12 million in revenue. By 2024 that figure had risen to $91 million, a CAGR of about 66%. For 2025 management is guiding to between CAD $120-$135 million, underpinned by a record order backlog of over $2 billion.

Gross margins expanded to 56% in the second quarter of 2025, up 500 basis points from the previous year, reflecting the higher mix of batteries and field services. Adjusted EBITDA slipped temporarily to $4.7 million as the company invested in new facilities and integration costs from the 3D at Depth acquisition, but underlying cash generation remains strong. Kraken ended Q2 2025 with $32.9 million in cash and $19 million in debt, down from $58.5 million at year-end 2024.

Capacity is about to expand dramatically. Kraken’s new Halifax facility, a 60,000-square-foot manufacturing plant, will triple its subsea battery output by late 2025 to a range of $200–250 million in annual capacity. When combined with its German operations, the company will operate more than 150,000 square feet of production space across North America and Europe, enough to support several parallel defense programs. Management expects the new capacity to be fully utilized within two years, driven by the ramp of Anduril’s Rhode Island and Australian factories.

If Kraken executes on its current trajectory, revenue could reach $500 million by 2027 and potentially $1 billion by the end of the decade. Operating margins, already north of fifteen percent, could expand toward twenty-five percent as fixed overhead is absorbed by higher throughput. These are conservative assumptions relative to the growth curves of similar defense technology suppliers.

Kraken Robotics: Scaling Profitably after a Transition from Net Cash to Moderate Leverage

Kraken Robotics was one of the fastest-growing defense technology firms over the past three years. Between 2021 and 2024, revenue rose at an impressive 52.7% compound annual rate, and the company turned profitable for the first time. But the first half of 2025 tells a different story. The latest results show weaker sales, lower margins, and a shrinking cash balance. Kraken’s long-term technology edge remains intact, but near-term execution challenges have replaced the “hyper-growth” optimism.

Sales Momentum Has Stalled

For the six months ending June 2025, Kraken generated CAD $42.5 million in revenue, down 3% from last year’s $43.6 million. That’s a sharp contrast to the 30-40% growth pace management guided for the full year. To hit its 2025 target of CAD $120–135 million, Kraken will need roughly $85 million in the second half, twice what it delivered in the first six months. Hitting that number will require flawless execution and a rapid ramp-up of new defense contracts.

Most of the slowdown came from the product division, where sales fell 27% year-over-year as the large Canadian Navy RMDS program wound down. While second-quarter revenue rose 13% from the weak first quarter, it only softened the overall decline.

The sonar (SAS) segment barely grew, up just 3%, though Kraken did win a $13 million new order for ten units from a foreign navy. The SeaPower battery business, once the main driver, also cooled as deliveries slipped into later quarters. The one bright spot was Robotics-as-a-Service (RaaS), which jumped 180% year-over-year in Q2 after the 3D at Depth acquisition. Services now account for about 37% of total revenue, up from 15% last year, helping reduce dependence on lumpy hardware sales.

Profitability Under Pressure

After celebrating a strong profit in 2024, Kraken slipped back into the red. It reported a net loss of CAD $0.5 million in the first half of 2025, compared with a $4.8 million profit a year earlier. Operating margins also fell: EBITDA margin declined to 18% from 22%, showing about 400 basis points of compression.

The main reason is cost growth. Administrative expenses surged 74% to $15.9 million, with the workforce expanding 44% to 378 employees. The company is still integrating 3D at Depth and building capacity for future contracts, but these costs arrived before new revenue did. Until volume improves, profits will remain tight.

Cash No Longer “Fortress-Level”

At the end of June 2025, Kraken held CAD $32.9 million in cash, down 44% from $58.5 million at the end of 2024. The decline mainly reflects the $23.5 million cash payment for 3D at Depth, plus ongoing investment in the new Nova Scotia battery plant. With about $19 million of debt, Kraken no longer has a net-cash position. Liquidity remains adequate, but the margin of safety is smaller.

Total assets rose to $178.8 million, boosted by the acquisition, construction work, and a buildup of inventories tied to large projects like the Ghost Shark underwater vehicle. Working capital sits near $95 million, yet much of it is tied up in receivables , 80% of which come from just two customers. That concentration raises short-term payment risk if deliveries are delayed.

Operating cash flow for the first half was only $1.5 million, while capital spending reached $7.6 million for the new battery facility, leaving free cash flow slightly negative. Contract liabilities rose sharply to $11 million from $1 million a year earlier, reflecting prepayments on undelivered orders. This adds pressure to meet delivery schedules in the second half.

Guidance Looks Ambitious

Management reaffirmed its full-year guidance of CAD $120–135 million in revenue and $26–34 million in adjusted EBITDA, but based on first-half performance, those numbers look hard to reach. To get there, Kraken must nearly double revenue in H2 while restoring profit margins. The market appears cautious: after factoring in weaker results and a thinner balance sheet, a more realistic fair-value range is CAD $4.50–$5.00 per share, down from the previous $6.50 target. If second-half results disappoint, downside risk could reach 25–35%.

Long-Term Outlook Still Intact

Despite short-term softness, Kraken’s long-term story remains appealing. Its SeaPower pressure-tolerant batteries and synthetic-aperture sonar systems are still essential technologies for next-generation unmanned underwater vehicles. The RaaS business is beginning to add recurring, high-margin revenue, which could stabilize cash flow once scale improves. The key will be execution , converting its large backlog into deliveries, controlling administrative costs, and efficiently ramping the new battery plant, which is expected to contribute $8–12 million in annual EBITDA once partially utilized in 2026.

MARKET OPPORTUNITY:

Kraken Robotics represents one of the most asymmetric small-cap opportunities in global defense, an undersea technology supplier positioned to scale alongside Anduril Industries, the $30 billion defense hyperscaler redefining autonomous warfare. While most investors chase aerial drones, the next frontier is subsea, where strategic deterrence, critical infrastructure, and communications intersect.

The Structural Opportunity

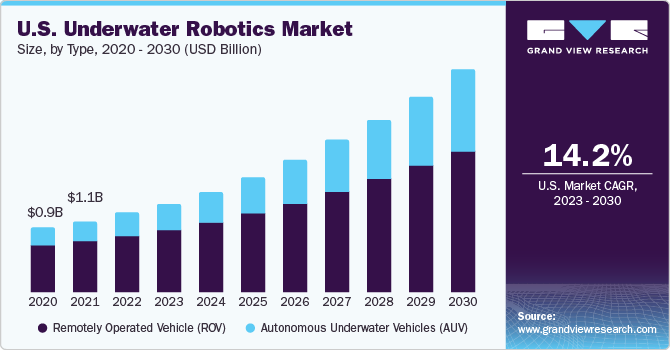

The global underwater robotics market, spanning defense, energy, and subsea infrastructure, is projected to grow from approximately $5 billion in 2024 to $12–13 billion by 2030, an estimated 14–16 % CAGR.

While this growth rate appears moderate, it’s 5x faster than typical defense budgets, signaling a structural capital shift from crewed to autonomous platforms. The U.S. and its allies are racing toward 24/7 autonomous undersea capability by 2027, a doctrine that will require tens of thousands of subsea drones.

Kraken’s Monopoly-Like Position

Kraken is a leading supplier of advanced pressure-tolerant subsea energy systems, holding a dominant share in NAVSEA-rated battery solutions through its SeaPower batteries, as the only NAVSEA-certified, pressure-neutral batteries rated for 6,000 meters. They deliver 2–3x higher energy density than competitors and use no Chinese materials, a decisive advantage under current defense restrictions. Combined with Kraken’s Synthetic Aperture Sonar (SAS) technology, offering significantly higher resolution (centimeter-scale imaging) at roughly half the cost of legacy systems, the company owns the enabling layer of the subsea autonomy stack.

The Anduril Catalyst

Anduril’s next-gen platforms, Dive-LD, Dive-XL (Ghost Shark), and Copperhead, all run on Kraken’s SeaPower batteries and sensors.

- Dive-LD units include roughly CAD $1–2 million of Kraken hardware each.

- Dive-XL (Ghost Shark) units: CAD $8–10 million per drone.

- Copperhead smart torpedoes: CAD $100–250k in Kraken content.

As Anduril ramps up production across its Rhode Island and Australian factories, each targeting hundreds of subsea drones per year, Kraken’s revenue potential from Anduril alone exceeds its current market capitalization. Switching suppliers is practically impossible: NAVSEA recertification would take 18–24 months, far too long under the U.S. Navy’s “maximum readiness by 2027” mandate.

The Broader Ecosystem

Beyond Anduril, Kraken supplies Huntington Ingalls (HII) for the REMUS series and multiple NATO navies (Canada, Norway, Turkey, Germany, and the UK). A second major XL-UUV customer announcement is expected within 12 months, a key diversification catalyst. In commercial markets, Kraken’s 3D at Depth acquisition opens fast-growing subsea inspection verticals such as offshore wind, subsea cables, and digital-twin asset mapping, projected to grow over 20% annually through 2030.

The Asymmetry

This convergence of defense urgency, technological lock-in, and hyperscaler leverage creates nonlinear upside. Kraken’s 2025 revenue is projected at ~CAD $120–130 million, yet its potential exceeds CAD $1 billion by 2028 if Anduril’s capacity is fully utilized.

Competitive Landscape Assessment

The underwater robotics market remains highly fragmented, dominated by large incumbents such as Teledyne Marine, Kongsberg Maritime, Thales, and Exail, which primarily serve government and industrial clients through slower, legacy platforms.

While these players benefit from scale and long-standing defense relationships, they struggle with innovation speed, cost efficiency, and integration across sensing, energy, and autonomy systems. Kraken Robotics stands out as the only fully integrated challenger, offering best-in-class synthetic aperture sonar, NAVSEA-certified subsea batteries, and 3D LiDAR capabilities under one platform.

This vertical integration enables Kraken to deliver faster, cheaper, and more modular solutions with interoperability across multiple OEMs and navies, positioning it as the agile disruptor redefining the cost-performance curve in subsea autonomy.

Kraken Competitive Advantages:

- Technological Moat: 10-year R&D investment; 10x superior SAS resolution vs. next-best competitor; only pressure-tolerant battery with no switching costs once integrated.

- Cost Advantage: Kraken charges ~30-40% less than Teledyne/Kongsberg for equivalent performance; pricing reflects manufacturing efficiency and direct-to-customer model.

- Integration Superiority: Vertical integration (SAS + batteries + platforms + services) enables differentiation; competitors cannot match; customers receive integrated solutions vs. best-of-breed components.

- Speed & Agility: 24-month product cycles vs. 3-5 years for incumbents; rapid iteration capability valued in defense modernization context.

- Customer Stickiness: Once integrated into the UUV platform and deployed operationally, switching costs are prohibitive (re-certification, re-integration, testing delays violate US Navy 2027 deployment mandate).

Competitive Vulnerabilities:

- Scale Disadvantage: Teledyne, Kongsberg, Thales have 10-50x revenue scale; can cross-subsidize markets and invest in R&D faster.

- Customer Concentration: Anduril represents 35-50% of the forward pipeline; major loss would be catastrophic.

- Execution Risk: New battery facility and services acquisition require flawless execution; manufacturing ramp or integration failures could disappoint investors.

- In-Housing Threat: Large primes (Northrop, Huntington Ingalls, L3Harris) could develop alternative batteries/sonar internally post-2027; though switching costs make this unlikely.

PIPELINE / BACKLOG:

Kraken Robotics’ latest updates show that while short-term sales have softened, the company’s long-term outlook remains strong. As of April 2025, Kraken reported a CAD $2 billion sales pipeline, more than double the $900 million reported a year earlier. This growth reflects rising demand following its partnership with Anduril Industries and its expanding role in underwater defense and energy markets.

Pipeline and Backlog Strength

Of the $2 billion pipeline, around $350–450 million sits in advanced bid stages with a 40–60% chance of closing, while another $600–800 million is in proposals and $750–850 million in early discussions. On average, about 25% is expected to convert, giving Kraken an estimated $500 million in potential bookings over the next few years.

Kraken’s current backlog is estimated at CAD $250–350 million, made up of confirmed contracts and purchase orders that will deliver revenue gradually through 2027. This includes the ongoing Anduril Ghost Shark program, new NATO navy projects, and service agreements. While early 2025 revenue was uneven due to the completion of the Canadian Navy RMDS program, deliveries are expected to accelerate in the second half as new contracts ramp up.

Recent Wins and Diversification

In September 2025, Kraken announced $13 million in new orders, including ten high-end sonar systems and battery contracts for customers in the U.S., Norway, and Turkey. These orders will be delivered in 2026 and help reduce reliance on Anduril, which still represents roughly 40–50% of the pipeline.

At the same time, the SeaPower battery division hit record quarterly revenue, while service revenue, boosted by the 3D at Depth acquisition, rose 180% year over year in Q2 2025. This mix shift toward recurring service revenue is a positive step that should make Kraken’s cash flows more stable in future years.

Ghost Shark: The Main Growth Engine

Kraken’s biggest opportunity lies in its partnership with Anduril on the Ghost Shark autonomous submarine program, a five-year, AUD $1.7 billion project for the Australian Defence Force. Each Ghost Shark unit uses Kraken sonar and batteries worth roughly CAD $11–16 million.

Production starts in 2026 and scales through 2030, potentially generating $130–200 million per year for Kraken at peak. Even under conservative assumptions, Ghost Shark could add $300–400 million in cumulative revenue over five years, and up to $1 billion if production expands or new variants are introduced.

LEADERSHIP:

Kraken’s leadership transition in 2022 from founder Karl Kenny to CFO-turned-CEO Greg Reid marked the beginning of a new operational era. Reid has emphasized disciplined capital allocation and lean execution. Despite funding expansion through several equity raises, per-share revenue has grown at a 36% annual rate since 2020, proving that dilution has been more than offset by value creation.

Reid’s approach contrasts sharply with the typical high-burn defense startup culture. He is known for flying coaches and refusing lavish compensation, setting a tone of frugality that has percolated throughout the organization. Complementing this fiscal prudence is a board of directors with rare strategic depth. Vice Admiral Michael J. Connor, former Commander of US Submarine Forces, sits on the board and brings unparalleled access to naval decision-makers. Connor’s presence effectively embeds Kraken into the US undersea warfare establishment, a quiet but powerful form of lobbying.

While Reid’s experience running a multi-billion-dollar enterprise is untested, his background in finance ensures operational discipline. As Kraken grows, he may eventually recruit or hand off leadership to a seasoned defense executive, but for now the combination of prudence and execution focus appears to be serving shareholders well.

VALUATION:

Multi-Year Asymmetry Built on Nonlinear Scaling

At $4.50 USD (CAD $5.77), Kraken Robotics trades at a market capitalization of CAD $1.77 billion (USD $1.47 billion). The stock screens are expensive versus traditional defense peers, but its valuation compresses rapidly if Kraken executes its scaling roadmap with Anduril and NATO navies.

Kraken’s core investment asymmetry lies in its nonlinear operating leverage. While consensus models assume a gradual, linear trajectory, Kraken’s growth potential depends on a binary shift from prototype supply to full-scale production, as Anduril ramps up autonomous subsea drones at multiple facilities worldwide.

Revenue Scenarios

| Scenario | Description | FY2028 Revenue (USD) | FY2028 Revenue (CAD) | CAGR (2025–2028) |

| Analyst Base | Reflects current contracts + backlog only | $200M | $270M | 31% |

| Execution Case | Adds Anduril Australia + new NATO orders | $450M | $610M | 52% |

| Strategic/Bull Case | Full Anduril global scaling, second XL-UUV customer | $730M | $1.0B | 72% |

Valuation Sensitivity Matrix (Fair Value per Share in USD)

Assumes fully diluted share count ≈ 270M; EV ≈ Market Cap (low net debt); Exchange rate 0.78 USD/CAD

| FY2028 Revenue (USD) | 4x P/S | 5x P/S | 6x P/S | 8x P/S |

| $200M (Analyst Base) | $2.96 | $3.70 | $4.44 | $5.92 |

| $450M (Execution Case) | $6.66 | $8.33 | $9.99 | $13.32 |

| $730M (Bull Case) | $10.81 | $13.51 | $16.22 | $21.62 |

Current price: $4.50 USD

→ Base Case Fair Value: ~$5.00–6.00 USD (modest rerating on guidance execution)

→ Bull Case Potential: $10–13.5 USD (120–200% upside)

→ Stretch Case (8x P/S): $21+ USD (long-term 4x multibagger potential)

Interpretation

- Analyst Base ($200M revenue): Market is pricing 7x forward P/S — fair for near-term execution but leaves limited rerating room.

- Execution Case ($450M): Realistic if Anduril’s Rhode Island and Australia plants operate near full capacity by 2027–2028. Kraken could command a 5–6× sales multiple, driving 100%+ upside.

- Strategic/Bull ($1B CAD): Reflects Kraken’s transformation into a global subsea defense supplier, supported by multiple production lines, NATO adoption, and 25%+ operating margins. Even a 4× sales multiple would justify $10–11.50 USD per share, a 150–200% revaluation.

Asymmetric Payoff and Downside Buffer

| Metric | Upside (Base → Bull) | Downside (Execution Miss) | Asymmetry Ratio |

| Price Change | +130% | –20% | ~6.5 : 1 |

Kraken offers one of the most asymmetric setups in small-cap defense: for every dollar of downside, investors are positioned for roughly $6.50 in upside under realistic scaling assumptions. The large divergence between consensus ($200M) and full-scale potential ($1B) reflects the market’s underappreciation of defense hyperscaling dynamics.

Valuation Takeaway

Kraken’s valuation hinges on time compression and operating convexity, the transition from low-volume prototyping to scaled production amplifies both revenue and margins. In simple terms, once Kraken moves from building prototypes to mass-producing subsea drones, sales and profits could accelerate sharply, making the company much more valuable in a short period of time.

Yiazou models what’s inevitable once production ramps, potentially $1B in revenue and 4–6x P/S by 2028.

At today’s $4.50 price, Kraken is valued as a niche supplier. Within three years, it could be re-rated as a strategic defense manufacturer. If execution aligns with Anduril’s ramp, fair value expands toward $10–13.5 USD with multi-bagger potential beyond.

→ Rating: BUY (Speculative Growth)

12-Month Target: $6.00–7.00 USD (+40–55%)

24-Month Target: $8.50–10.00 USD (+90–120%)

2028 Target (Strategic Scaling): $10.00–13.50 USD (+150–200%)

Asymmetry Ratio: 6.5x (Best-in-Class)

RISK ASSESSMENT:

Kraken Robotics operates in a high-growth but high-risk segment of the defense industry. While its technology and backlog provide a strong foundation, investors should understand the main risks that could affect future performance and how management is addressing them.

1. Heavy Reliance on Anduril

The single biggest risk is customer concentration. Anduril is estimated to represent 40–50% of Kraken’s forward sales pipeline, equal to nearly CAD $1 billion of future opportunities. Losing this relationship could cut annual revenue by over CAD $100 million and severely damage the business.

However, the risk is partly mitigated by the deep integration between the two companies. Kraken’s SeaPower batteries are unique in the market and critical for Anduril’s Ghost Shark program, replacing them would require years of testing and certification. Recent $13 million in non-Anduril contracts and new NATO customers also show that diversification is underway. Management has confirmed it is pursuing a “second XL-UUV customer” to further reduce dependency.

Probability: Low (10–15%)

Impact: Very high if realized

2. Execution Risk at the Nova Scotia Battery Facility

Kraken is investing CAD $60–80 million in a new manufacturing plant that must reach at least 50% utilization by 2026 to justify its cost. Any delay or cost overrun could pressure margins and cash.

The risk is reduced by early construction progress, technical transfer from Kraken’s German operations, and sufficient equity funding from the recent CAD $115 million raise. Demand for the company’s subsea batteries is already strong, suggesting little risk of underutilization.

Probability: Medium (25–35%)

Impact: Moderate

3. Competitive Threats from Larger Defense Companies

Big defense primes like Teledyne, Kongsberg, and Thales could accelerate their underwater sonar and energy solutions, using larger R&D budgets to compete on price or scale.

Kraken’s defense lies in its 10-year technology head start, patented SAS algorithms, and unique pressure-neutral battery design. Many competitors have instead chosen to partner with Kraken rather than replace it. With the underwater robotics market growing more than 15% annually, there’s room for several players.

Probability: Medium (30–40%)

Impact: Moderate

4. Future Dilution and Capital Raises

The 2025 CAD $115 million equity raise diluted shares roughly one-third. Further raises could erode per-share value if not matched by accretive returns.

This is mitigated by the company’s two-year funding runway and management’s history of using capital for productive, high-ROI projects such as the new battery facility.

Probability: Medium (40–50%)

Impact: Moderate

5. Liquidity and Low Trading Volume

Average daily volume for Kraken Robotics totals roughly 2.7 million shares across all exchanges, split between ~1.14 million on the TSXV (PNG.V) and ~1.57 million on the U.S. OTC (KRKNF). Thin trading can amplify price swings and make large buy or sell orders move the stock dramatically. Institutional investors may hesitate to build sizable positions, limiting near-term valuation expansion.

Liquidity should improve if Kraken uplists to the Toronto main board or NASDAQ, but until then, investors must expect wider bid-ask spreads and higher volatility.

Probability: High (70%+)

Impact: Moderate (short-term valuation ceiling, higher volatility)

6. Other External Risks

Revenue remains lumpy due to large contract timing, and macro events such as defense-budget cuts or export restrictions could affect demand. However, sustained geopolitical tensions and NATO’s 2%-spending rule make drastic cuts unlikely.

Bottom Line

Kraken’s risks cluster around execution, concentration, and liquidity. The business is technologically strong but still small and dependent on a few key partners. A successful NASDAQ uplisting, continued diversification, and disciplined capital use will be critical to reducing volatility and unlocking a broader institutional investor base.

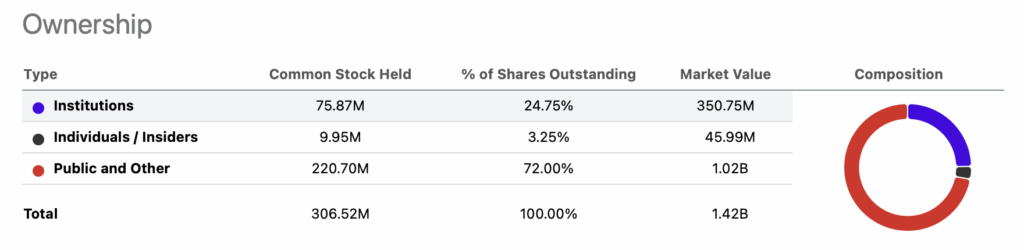

OWNERSHIP & LIQUIDITY:

Kraken Robotics’ ownership structure reflects a healthy mix of insider commitment and growing institutional confidence, though liquidity remains a constraint for larger investors.

Insider Holdings and Activity

As of October 2025, insiders collectively hold around 10.6 million shares, or 3.25% of outstanding stock. CEO Greg Reid owns 8.2 million shares (3.1%), though he sold roughly 810,000 shares in June 2025 at about $2.19 USD. The timing, before a massive run-up, suggests portfolio diversification rather than a loss of confidence. By contrast, CFO Joseph MacKay and CTO David Shea made open-market purchases in January 2025 at prices near $1.50–$2.00 USD, signaling conviction in Kraken’s outlook.

Overall, insider trading trends lean neutral-to-positive. The CEO’s sale might appear cautious, but the combination of early-year insider buying and strong post-sale price appreciation suggests management alignment with long-term growth.

Institutional Ownership and Trends

Institutional investors now hold an estimated 24.8% of total shares, up 33% year-over-year. Ownership is dominated by Canadian growth managers, led by Mawer Investment Management (10.8%) and PenderFund Capital (8.5%), both known for their disciplined, long-term approach. Other holders include Fidelity and Storebrand, expanding Kraken’s reach into global small-cap portfolios.

This institutional mix provides validation of Kraken’s fundamentals but also highlights an opportunity: limited U.S. institutional participation, a gap that could close once the company uplists to NASDAQ, broadening investor access and liquidity.

Share Structure and Dilution

Kraken’s share count expanded from 157 million in 2023 to about 261 million by October 2025, mainly from the CAD $115 million equity raise completed in August. The raise increased shares by roughly 30% but was priced at CAD $2.52–2.68, now well below the current CAD $5.81 market price, a 118% premium that validates market acceptance.

While dilution was significant, proceeds are being directed toward high-return projects such as the new Nova Scotia battery facility and the 3D at Depth acquisition, both expected to enhance long-term cash flow and scale.

Liquidity and Trading Profile

Kraken trades primarily on the TSX Venture Exchange (PNG) and the OTCQB (KRKNF) in the U.S. Average daily volume is roughly 1 million shares (~USD $4.6 million), with bid-ask spreads of about 1–2%, adequate for retail and mid-sized investors but thin for larger funds. Positions of $1–5 million can be built easily, while those exceeding $15 million would likely move the stock without coordination.

A NASDAQ uplisting, expected between Q4 2025 and Q1 2026, would likely triple or quadruple liquidity, attract more U.S. institutions, and potentially lift valuation multiples by 20–40%. Kraken already meets all listing criteria, price, capitalization, and equity, making approval a matter of timing rather than qualification.

CATALYSTS:

Near-Term Catalysts (Q4 2025 – Q2 2026)

Q3 2025 Earnings Release (Dec 2025)

- Impact: ★★★★☆ (High – critical for guidance confirmation)

- Expectations: Revenue CAD $26–29M; EBITDA CAD $4–6M

- Bull Case: Revenue > $28M and margin rebound → validates growth trajectory

- Bear Case: Revenue < $25M or margin compression → guidance risk

- Watch: Updated 2025 guidance, backlog, and order commentary

Nova Scotia Battery Facility Commissioning (Q4 2025)

- Impact: ★★★☆☆ (Medium)

- Expected: Press release confirming operational status and utilization goals

- Bull Case: Early launch and strong demand visibility → de-risks 2026 targets

- Bear Case: Delay into Q1 2026 or cost overruns → pressure on cash and margins

NASDAQ Uplisting Filing (Q4 2025 – Q1 2026)

- Impact: ★★★★☆ (High)

- Catalyst: Application once price >$4.00 USD maintained 90 days

- Expected: Q4 2025 filing, Q1 2026 approval

- Market Impact: +5–10% liquidity-driven revaluation; broader U.S. investor access

Anduril Ghost Shark First Delivery (Jan 2026)

- Impact: ★★★★★ (Critical – program validation)

- Expected: Joint press release with Australian Navy confirming delivery

- Bull Case: On-time delivery and follow-on orders → +15–25% share upside

- Bear Case: Technical or timing delay → –20–30% downside

FY2025 Earnings (May 2026)

- Impact: ★★★★☆ (High)

- Expectations: Revenue $120–135M; EBITDA $26–34M

- Bull Case: Top-end results with 2026 guidance > $170M revenue → strong rerating

- Bear Case: Missed targets → credibility hit

2026 Guidance Update (May 2026)

- Impact: ★★★★☆ (High)

- Expected: Revenue $160–185M; EBITDA $38–48M (22–26% margin)

- Key Metric: Continued service revenue growth (target 40%+ mix by 2027)

Conclusion

Kraken Robotics offers a rare pure-play opportunity in subsea defense and autonomy. The investment thesis is strong but execution risk remains.

- Allocating 5-10% in high conviction portfolios captures asymmetric upside from the Anduril ramp and technology moat.

- Stagger purchasing and actively monitor operating results to manage risk.

- Employ disciplined risk management via stop-losses and position sizing.

- Stay alert for news flow regarding NASDAQ uplisting and Anduril battery development risk.

This strategy balances growth potential with fundamental and execution risk, appropriate for sophisticated investors in growth and frontier technology sectors.

Kraken fits best within a speculative growth or asymmetric opportunity sleeve, similar to early-stage defense compounders like Palantir.

While the stock may remain volatile due to low liquidity and event-driven catalysts, disciplined accumulation near current levels offers an exceptional 6.5:1 asymmetry ratio between upside potential and downside risk.

Investors with multi-year horizons and tolerance for short-term volatility are positioned to benefit most as Kraken transitions from niche supplier to global defense infrastructure standard.