Over the past year, a few Bitcoin miners like IREN Limited (IREN) and TeraWulf (WULF) have seen their stock prices explode, some rising several hundred percent. Why? Because they shifted part of their infrastructure from mining Bitcoin to powering artificial intelligence (AI) data centers.

This trend is redefining what it means to be a miner. These companies are no longer just chasing Bitcoin rewards; they’re becoming digital energy utilities, turning megawatts of power into either Bitcoin or compute for AI.

And this is where CleanSpark (CLSK) quietly stands out.

While others have captured headlines with early AI hosting deals, CleanSpark has built something more fundamental: a massive, owned power network and one of the most efficient Bitcoin mining fleets in the world. It hasn’t yet made a loud “AI pivot” announcement, but the groundwork is already there.

This article explains why CleanSpark might be the next big re-rating story in the Bitcoin-AI crossover, what makes it different from peers, and how it could realistically outperform companies that already rallied.

From Miner to Energy Company

CleanSpark is often called “America’s Bitcoin Miner,” and for good reason. The company has grown from a few hundred megawatts of power in 2021 to over 1 gigawatt (GW) of contracted power capacity across 33 sites in the United States, mainly in Georgia, Tennessee, Mississippi, and Wyoming.

To put that in perspective, 1 GW is enough electricity to power a city of roughly a million people.

The key difference between CleanSpark and other miners is that it owns its infrastructure. Many rivals lease or co-locate at third-party facilities, which means higher costs and less flexibility. CleanSpark buys land, builds substations, and operates everything itself. This vertical integration is what gives it control over speed, cost, and scalability.

In Bitcoin mining, power is everything. It’s the single largest cost driver. The company’s average electricity price is just $0.056 per kilowatt-hour, among the lowest in the industry. That cheap, stable energy gives it room to stay profitable even if Bitcoin’s price dips.

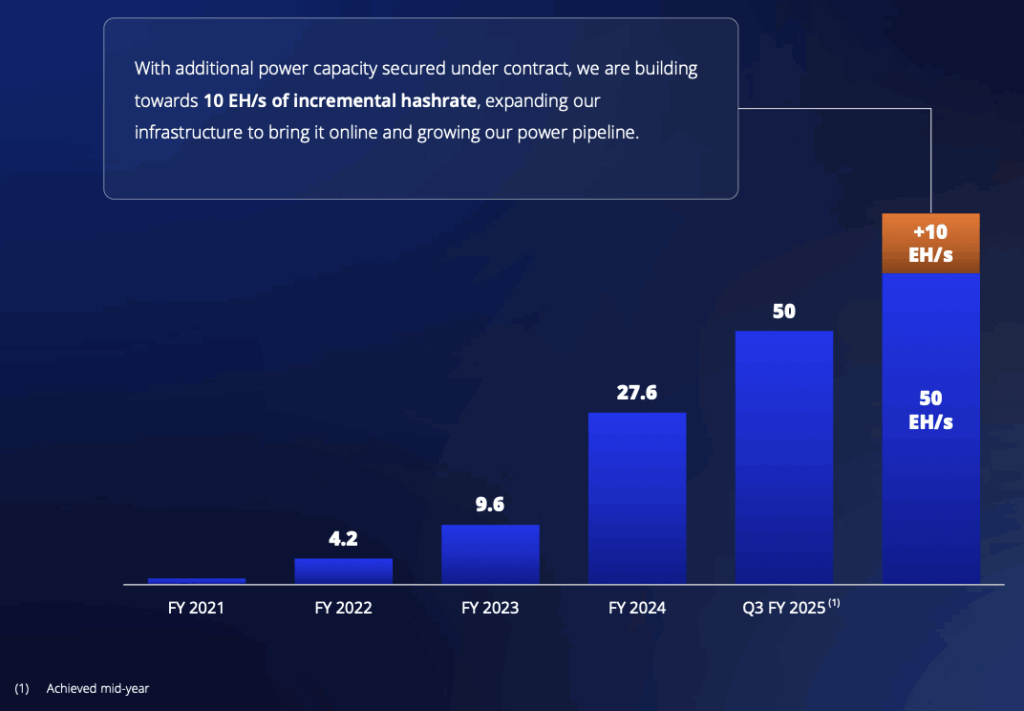

CleanSpark’s mining fleet now runs at 50 exahash per second (EH/s), essentially the computing muscle used to verify Bitcoin transactions, and it aims to reach 60 EH/s soon. That’s roughly 6–7% of the entire global Bitcoin network, a staggering level of scale for a single public miner.

The Scale and Efficiency Edge

The two things that make a miner profitable are scale and efficiency. CleanSpark has both.

Its fleet averages 16 joules per terahash (J/TH), a measure of how efficiently power turns into Bitcoin. Lower is better, and that number places CleanSpark near the global top. Many competitors still operate older machines that consume 25–30 J/TH or more.

Because of this efficiency, CleanSpark’s cost to mine one Bitcoin was around $44,800 in the last quarter, lower than its peers.

This isn’t a company scraping by on hype. It’s generating real profits:

- Q3 2025 revenue: $198.6 million (up 91% YoY)

- Net income: $257 million ($0.90 per share)

- Adjusted EBITDA: $377.7 million

And it achieved that without issuing new shares. Management hasn’t diluted shareholders since 2024. Instead, it funds expansion from operating cash flow and modest Bitcoin-backed loans.

That level of discipline is rare in crypto mining, where many competitors routinely sell stock to survive downturns. CleanSpark’s ability to scale without dilution shows operational strength that Wall Street has not fully recognized yet.

Bitcoin Mining Is Just the Beginning

While CleanSpark’s core business is still Bitcoin mining, its infrastructure was designed for something larger.

Each of its 33 data center sites is connected to utility-grade substations, uses immersion cooling systems, and runs on modular power blocks that can host any kind of high-density computing, not just ASIC miners.

That means these sites can eventually power AI and high-performance computing (HPC) workloads. In other words, the same power that runs Bitcoin rigs today could run GPU clusters for AI companies tomorrow.

This dual-use potential is where the opportunity lies.

The global shortage of AI data-center capacity is severe. Training large AI models like ChatGPT or running AI inference (processing millions of queries) requires vast amounts of power and cooling, resources miners already have.

By late 2025, analysts estimate global demand for AI power could exceed 40 gigawatts. That’s roughly 40 times CleanSpark’s current size, but the gap means hyperscale companies like Google, Meta, and Amazon will need to partner with existing operators who already control power and land.

This is precisely what happened to peers:

- TeraWulf (WULF): Signed a 10-year, 200 MW AI hosting deal with Fluidstack backed by Google. The contract is worth up to $8.7 billion.

- Cipher Mining (CIFR): Partnered with the same group for 168 MW in Texas, a 10-year deal valued around $3 billion.

- Applied Digital (APLD): Signed 250 MW in leases with CoreWeave (an AI cloud provider) worth $11 billion over 15 years.

- IREN Limited (IREN): Shifted away from mining to deploy 23,000 NVIDIA GPUs and secured $225 million in annual AI cloud contracts.

These announcements sent their stock prices vertical, many soaring between 300% and 900%.

CleanSpark hasn’t announced a deal yet, but it has quietly built the perfect foundation to follow the same path, just with more stability and lower risk.

Why CleanSpark Could Be the Next Big Re-Rating

1. Immersion Cooling Experience

CleanSpark was one of the first miners to deploy large-scale immersion-cooled hardware, where machines sit in a dielectric liquid that keeps them cooler and more efficient. This same technology is now used in AI data centers because GPUs generate even more heat than Bitcoin miners.

While others would need to retrofit, CleanSpark’s engineers already know how to run immersion systems at scale. That’s a major technical advantage if the company decides to allocate part of its 1 GW power to AI hosting.

2. Strategic Power Portfolio

CleanSpark’s power is all in the United States and spread across politically friendly, energy-rich states. Georgia and Wyoming have become major data-center hubs with strong grid reliability.

Each of these sites connects to high-voltage substations that can feed new compute clusters without massive new infrastructure. This makes CleanSpark an attractive partner for AI firms that need power-ready land near fiber routes and metro areas like Atlanta.

Because it owns the land, CleanSpark can repurpose it faster than competitors relying on third-party hosts.

3. Speed of Execution

Perhaps CleanSpark’s most underrated strength is execution speed.

When it acquired new land in rural Georgia in 2025, it built and energized an immersion-cooled facility within five weeks. In mining, that speed is unheard of.

This means when the company decides to build an AI-specific data center, it can likely deploy in months, not years, while others are still designing blueprints.

4. Financial Flexibility

CleanSpark ended the last quarter with:

- $1.5 billion in Bitcoin

- $34.6 million in cash

- $820 million in debt (most of it 0% convertible notes)

- $400 million in new Bitcoin-backed credit lines

That gives it over $1.9 billion in liquidity to expand without issuing new stock.

Compare that to smaller peers who need to raise money through equity every time they build a new site. CleanSpark’s balance sheet gives it optionality, it can fund the first AI campus internally while keeping control.

5. Valuation Discount

Even after its rally this year, CleanSpark trades around $22/share, giving it a market cap near $6.25 billion.

CLSK trades at a forward P/S of just 5.5x despite projected 2026 revenue of $1.13B (+45% YoY) and consistent profitability. Its forward P/E of 17x is nearly half that of growth peers in the AI-infrastructure and data-center space, which average 30–35x.

CLSK’s 55% gross margins, self-funded expansion, and $1.5B Bitcoin treasury make it one of the few miners generating real free cash flow. Yet, it remains priced like a cyclical miner rather than a scalable compute utility. A re-rating to peer multiples implies 50–80% upside, making it one of the market’s most mispriced AI-energy hybrids.

Comparing the Competition

To understand CleanSpark’s opportunity, let’s see what the others are doing and what it tells us about market psychology.

| Company | Power (MW) | AI/Hosting Deals | Key Advantage |

| CleanSpark (CLSK) | 1,000+ | None yet (expected) | Vertically integrated, lowest cost, fastest builder |

| IREN Limited (IREN) | 2,900 | $225M AI contracts, 23K GPUs | Early AI pivot, renewable power |

| MARA (MARA) | 1,100 | Developing HPC/AI sites | Scale and treasury (52K BTC) |

| TeraWulf (WULF) | 1,150 | Google/Fluidstack $8.7B deal | Renewable energy + AI contracts |

| Cipher (CIFR) | 750 | Fluidstack $3B deal | Large U.S. AI partnership |

| Applied Digital (APLD) | 250 | CoreWeave $11B leases | Pure-play AI data centers |

| Hut 8 (HUT) | 1,000 | 4 new AI campuses | Hybrid Bitcoin + HPC strategy |

| Bitfarms (BITF) | 650 | AI-ready site in Pennsylvania | Strong hydro power, early retrofit |

Every one of these companies saw massive stock gains once it linked its narrative to AI hosting.

The irony? CleanSpark’s technical and financial foundation is stronger than many of them, it just hasn’t yet told the AI story.

That’s the asymmetry. Investors get exposure to a top Bitcoin producer now, with a free call option on the AI pivot later.

The Technical Setup for a Future Rally

Let’s talk about what could actually make CleanSpark’s stock “go parabolic” the way peers did.

Catalyst 1: First AI or HPC Partnership

The day CleanSpark announces a power-lease agreement, even for a modest 50–100 MW AI campus, expect the market to respond instantly.

If TeraWulf and Cipher secured multi-billion-dollar deals and saw valuations explode, CleanSpark could easily experience the same once it locks in a top-tier partner (Google, Meta, Amazon, or an AI startup).

Catalyst 2: Bitcoin Halving Cycle

Bitcoin has already traded above $100,000 for several months, signaling the start of the post-halving expansion phase.

CleanSpark’s cost per BTC mined (~$44,800) positions it to expand margins dramatically as weaker miners exit.

With network difficulty consolidating and BTC stable in six figures, revenue and cash generation could double before any AI income arrives.

Catalyst 3: Regulatory and Political Support

New U.S. laws like the GENIUS Act and Clarity Act are bringing positive regulation to digital assets and U.S. mining. CleanSpark, operating entirely domestically, benefits from these policy tailwinds.

It’s even been cited as an example of “responsible mining”, a reputation that could make it a preferred AI partner for companies under ESG pressure.

Catalyst 4: Institutional Adoption

Bitcoin ETFs are now mainstream. Large funds need ways to play the digital-asset economy without directly holding coins. CleanSpark offers that exposure, but with profitability and infrastructure, not speculation.

If CleanSpark signs its first AI deal, expect institutional inflows similar to what drove IREN Limited and MARA higher.

Risk Factors to Watch

No opportunity is without risk, and subscribers should be aware of these key ones:

1. Bitcoin Price Volatility

CleanSpark still earns most of its revenue from mining. A deep Bitcoin correction (say below $60K for an extended period) could compress margins and delay expansion. But with an average cost of $44K per BTC, CleanSpark would remain profitable even through moderate downturns.

2. Timing of the AI Pivot

If the company waits too long to announce or build an AI campus, the market could lose patience and reward faster-moving peers. Execution speed will matter.

The good news: CleanSpark’s proven ability to energize new sites within weeks means it can move quickly once the decision is made.

3. Competition for AI Deals

AI hosting is becoming a crowded field. CoreWeave, Fluidstack, and hyperscalers are bidding aggressively for capacity. CleanSpark’s advantage is its scale and flexibility, but margins could compress if too many players chase the same deals.

4. Capital Requirements

Although CleanSpark can fund the first HPC project internally, larger expansions may require financing. If Bitcoin prices drop simultaneously, raising capital could be more expensive.

Still, with $1.5B in Bitcoin holdings and $400M in available credit, the company has significant cushion.

The Bigger Picture: The Energy-to-Compute Shift

Every decade, a new infrastructure layer defines technology.

- In the 2000s, it was cloud computing.

- In the 2010s, it was mobile networks and hyperscale data centers.

- In the 2020s, it’s energy-driven compute, the intersection of power, chips, and intelligence.

Bitcoin miners were early to master this intersection. They know how to acquire cheap power, run high-density hardware, and scale efficiently. Now, the same playbook applies to AI.

CleanSpark already operates at the frontier of this model. It transforms energy into digital assets with unmatched efficiency. The next step, transforming that energy into AI compute, isn’t a leap. It’s a natural evolution.

And that’s the heart of the investment thesis: CleanSpark has already done the hard part. The power, land, cooling, and expertise are all in place. The company simply needs to decide how much of its capacity to allocate to AI. Once that happens, it won’t just be “America’s Bitcoin Miner.” It will be a digital-infrastructure powerhouse.

The Investment View

Let’s summarize the case for long-term investors.

Base Case (Next 6 Months)

CleanSpark expands to 60 EH/s, Bitcoin stays near $90K–$100K, margins remain above 50%, and the company continues to self-fund growth.

→ Stock re-rates to around $28–$32, up ~50% from current levels.

Bull Case

CleanSpark announces its first AI or HPC hosting partnership (50–100 MW), launching a new revenue stream. Market sentiment shifts, valuing it like IREN or WULF.

→ Potential 60–100% upside in 6-12 months.

Bear Case

Bitcoin retreats below $60K, delaying expansions and AI projects. Margins compress temporarily.

→ Stock consolidates but remains supported by tangible assets and Bitcoin treasury.

Conviction View

CleanSpark offers one of the clearest asymmetric setups in the market today:

- Downside: Backed by profitable mining and $1.5B in Bitcoin.

- Upside: Re-rating potential once AI hosting begins.

Conviction has been raised to medium-to-high following the latest quarterly results, which validated CleanSpark’s transition from a pure Bitcoin miner to a vertically integrated digital infrastructure operator. The company’s record profitability, 55% gross margin, and self-funded growth confirm operational excellence and scalability.

CleanSpark now earnigs the optionality bet ranking (1.5-4%) for portfolio weighting reflecting asymmetric upside from both Bitcoin exposure and future AI/HPC hosting potential. After waiting for execution proof, the Q3 2025 performance provided the confirmation needed to include CLSK as a structural position within the portfolio.

Final Thoughts

The market often rewards headlines before fundamentals. That’s why smaller miners with flashy AI announcements have surged faster than CleanSpark.

But over time, real scale, efficiency, and balance-sheet strength win. CleanSpark combines all three, and trades at a discount.

The company has proven it can mine Bitcoin profitably at massive scale, control costs, and expand quickly. What the market hasn’t yet priced in is its ability to monetize power beyond Bitcoin, to become part of the AI infrastructure economy.

When that realization hits, CleanSpark’s story could shift from “steady Bitcoin miner” to “U.S. compute infrastructure leader.”

In short:

CleanSpark is a power company disguised as a miner, with optionality to tap into the trillion-dollar AI energy boom.