SoFi’s Evolution from Lending to Full-Service Fintech

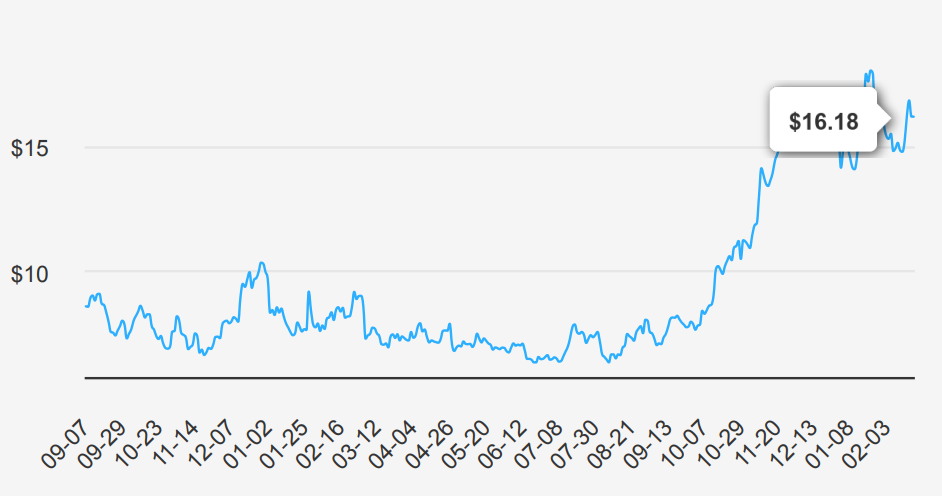

SoFi is a financial-services company that was founded in 2011 and is based in San Francisco. Initially known for its student loan refinancing business, the company has expanded its product offerings to include personal loans, credit cards, mortgages, investment accounts, banking services, and financial planning. The company intends to be a one-stop shop for its clients’ finances and operates solely through its mobile app and website. Through its acquisition of Galileo in 2020, the company also offers payment and account services for debit cards and digital banking. SoFi stock is currently trading at ~$16.18

EPS Rises to $0.05, 44% Revenue Growth Projected

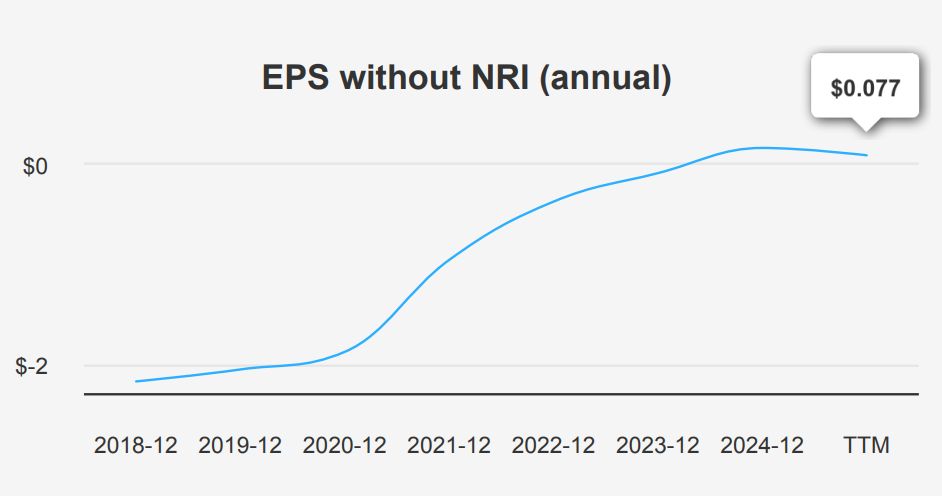

SoFi Technologies reported its earnings for the quarter ending December 31, 2024, with an EPS without non-recurring items (NRI) of $0.05, up from $0.049 in Q3 2024 and significantly higher than $0.02 in Q4 2023. This marks a steady improvement in profitability as the company continues to recover from negative EPS reported in early 2024. The EPS (Diluted) also showed a strong increase to $0.29, reflecting positive operational performance and the impact of financial strategies executed during the year. Revenue per share increased to $0.638 from $0.628 in the previous quarter, demonstrating consistent growth amidst a competitive market environment.

Looking forward, analysts estimate that SoFi’s revenue will grow from $3,228.51 million in 2025 to $4,654.66 million by 2027, with EPS expected to be $0.256 for FY 2025 and $0.490 for FY 2026. The financial services industry may grow at a steady rate over the next decade, providing a favorable backdrop for SoFi’s expansion plans. The next earnings release is on April 29, 2025, which should provide further insights into the company’s strategic direction and financial health.

At WACC at 19.87%—A Value Destruction Concern

Analyzing SOFI’s performance through its Return on Invested Capital (ROIC) and Weighted Average Cost of Capital (WACC) reveals critical insights into its financial efficiency and value creation. Over the past five years, SOFI has consistently shown a leveled ROIC, indicating that it has not been generating returns on its investments. In contrast, the median WACC over the same period stands at 6.81%, with a current rate of 19.87%, which suggests that the cost of capital is significantly higher than the returns generated.

This disparity between ROIC and WACC implies that SOFI is currently destroying value rather than creating it, as the capital employed is not yielding sufficient returns to cover its cost. Furthermore, the negative Return on Assets (ROA) and negative median Return on Equity (ROE) highlight inefficiencies in asset utilization and shareholder value generation. For SOFI to improve its economic value creation, it must enhance operational efficiency and strategic investments to boost its ROIC above its WACC, thereby creating positive shareholder value.

SoFi Stock: High Valuation, Insider Buying, and Revenue Declines—What’s Next?

SoFi stock presents several potential risks. The company’s current tax rate, which appears lower than average, may artificially boost earnings in the short term, raising sustainability concerns. Furthermore, the revenue per share has been declining over the past five years, indicating potential challenges in maintaining or growing revenue streams. The forward PE ratio being higher than the trailing PE suggests the market expects future earnings growth, despite recent declines in earnings. This disparity could set unrealistic expectations and may lead to volatility if earnings do not improve.

The stock price nearing a three-year high, coupled with a PS ratio close to a five-year peak, suggests that the stock may be overvalued. Investors may find the current valuation unattractive unless significant growth materializes. However, the recent insider buying transaction totaling 30,600 shares could indicate confidence from those within the company, which may reassure some investors. The Beneish M-Score of -2.77 suggests the company is unlikely to be manipulating earnings, a positive sign amidst the financial challenges. Overall, while there are optimistic signs, such as insider confidence and low manipulation risk, the high valuation and declining revenues present considerable risks that should be carefully weighed by investors.

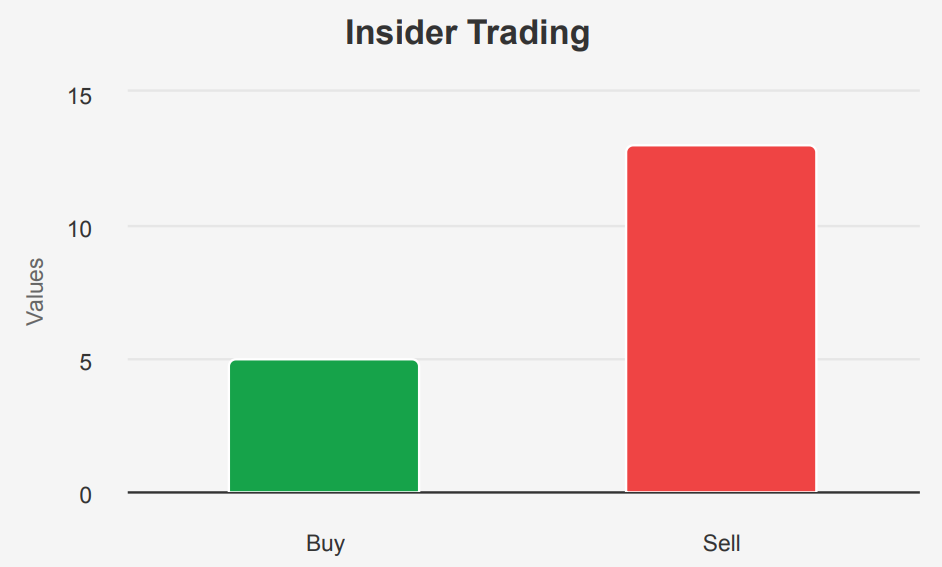

13 Sells, 5 Buys—Do Insiders Lack Confidence In SoFi Stock?

Over the past year, insider trading activity at SoFi stock has shown a trend towards selling rather than buying. In the last 12 months, 13 insider sell transactions have been compared to 5 buys, indicating a net selling trend. This pattern is more pronounced over shorter periods, with 10 sales and only 1 buy in the past 6 months and 6 sells against 1 buy in the last 3 months.

Insider ownership stands at 1.97%, which is relatively low, suggesting that insiders do not hold a significant portion of company shares. In contrast, institutional ownership is substantially higher at 44.80%, indicating strong interest from institutional investors.

The consistent selling activity might suggest that insiders are either capitalizing on stock price increases or have less confidence in the company’s near-term performance. However, the high level of institutional ownership could imply continued confidence in the company’s long-term prospects. Investors should consider these factors along with other financial indicators when evaluating SOFI’s stock.

42M Average Daily Volume For SoFi Stock, 39.89% Dark Pool Activity

SoFi stock exhibits notable liquidity in the market, with an average daily trading volume of approximately 42,179,430 shares over the past two months. This figure suggests robust investor interest and the ability of investors to enter and exit positions without significantly impacting the stock price.

The current daily volume stands at 34,848,171 shares, slightly below the two-month average, indicating a potential decrease in recent trading activity. However, this volume remains substantial, reflecting consistent engagement from market participants.

The Dark Pool Index (DPI) for SOFI is 39.89%. The DPI measures the percentage of trades executed in off-exchange venues, such as dark pools, which can offer insights into institutional trading behaviors. A DPI of 39.89% indicates that a significant portion of SOFI’s trading occurs outside of standard exchange mechanisms, possibly pointing to institutional interest.

Overall, SOFI maintains a healthy liquidity profile, supported by its considerable trading volume and active participation in dark pools. These factors contribute to its capacity to sustain active trading and price discovery, making it an attractive option for both retail and institutional investors seeking liquidity and market depth.

Lawmaker’s Bet on SOFI—A Sign of Confidence?

On January 2, 2025, Representative James Comer, a Republican member of the House, executed a significant purchase involving SOFI stock. The transaction, reported on January 10, 2025, was valued in the range of $1,001 to $15,000. This purchase was notable for its strong performance, achieving an excess return of 9.63% above the market benchmark, with the stock itself appreciating by 14.51% compared to the SPY’s gain of 4.88% during the same period.

This strategic move by Rep. Comer suggests an optimistic outlook on SOFI’s market potential, reflecting confidence in the company’s future growth prospects. His purchase underscores a trend of interest in fintech stocks, which have been increasingly appealing due to their innovative disruption in traditional financial services. This transaction highlights the importance of monitoring congressional trades as potential indicators of market trends and investor sentiment.

Disclosures:

Yiannis Zourmpanos has a beneficial long position in the shares of SOFI either through stock ownership, options, or other derivatives. This report has been generated by our stock research platform, Yiazou IQ, and is for educational purposes only. It does not constitute financial advice or recommendations.